Looking back on general industrial machinery stocks’ Q1 earnings, we examine this quarter’s best and worst performers, including John Bean (NYSE: JBTM) and its peers.

Automation that increases efficiency and connected equipment that collects analyzable data have been trending, creating new demand for general industrial machinery companies. Those who innovate and create digitized solutions can spur sales and speed up replacement cycles, but all general industrial machinery companies are still at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

The 14 general industrial machinery stocks we track reported a mixed Q1. As a group, revenues missed analysts’ consensus estimates by 1.5% while next quarter’s revenue guidance was 1.5% below.

Thankfully, share prices of the companies have been resilient as they are up 9.3% on average since the latest earnings results.

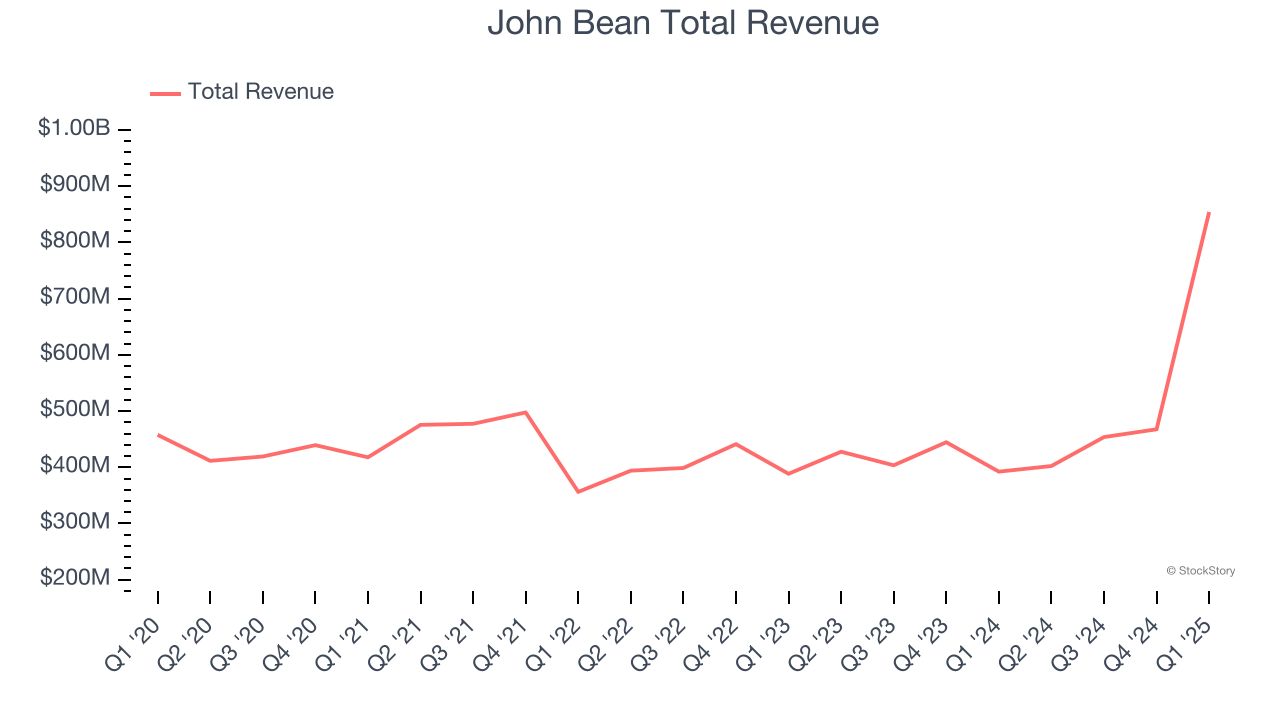

John Bean (NYSE: JBTM)

Tracing back to its invention of the mechanical milk bottle filler in 1884, John Bean (NYSE: JBT) designs, manufactures, and sells equipment used for food processing and aviation.

John Bean reported revenues of $854.1 million, up 118% year on year. This print exceeded analysts’ expectations by 2.6%. Overall, it was a very strong quarter for the company with an impressive beat of analysts’ EBITDA estimates and EPS guidance for next quarter exceeding analysts’ expectations.

"JBT Marel had a solid start to the year as we outperformed our first quarter expectations," said Brian Deck, Chief Executive Officer.

John Bean scored the fastest revenue growth of the whole group. Unsurprisingly, the stock is up 10.8% since reporting and currently trades at $118.73.

Is now the time to buy John Bean? Access our full analysis of the earnings results here, it’s free.

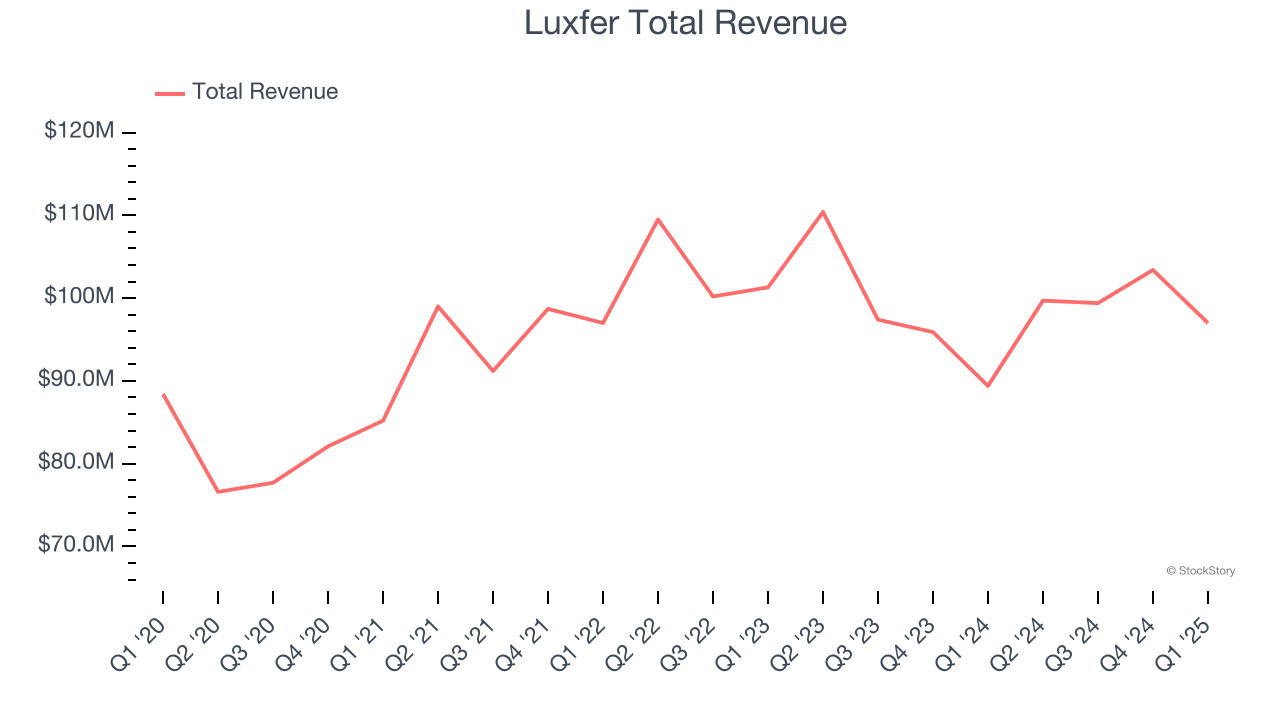

Best Q1: Luxfer (NYSE: LXFR)

With its magnesium alloys used in the construction of the famous Spirit of St. Louis aircraft, Luxfer (NYSE: LXFR) offers specialized materials, components, and gas containment devices to various industries.

Luxfer reported revenues of $97 million, up 8.5% year on year, outperforming analysts’ expectations by 11.9%. The business had an incredible quarter with an impressive beat of analysts’ EPS estimates and a solid beat of analysts’ EBITDA estimates.

Luxfer scored the biggest analyst estimates beat among its peers. The market seems happy with the results as the stock is up 19.6% since reporting. It currently trades at $11.95.

Is now the time to buy Luxfer? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: Icahn Enterprises (NASDAQ: IEP)

Founded in 1987, Icahn Enterprises (NASDAQ: IEP) is a diversified holding company primarily engaged in investment and asset management across various sectors.

Icahn Enterprises reported revenues of $1.87 billion, down 24.6% year on year, falling short of analysts’ expectations by 29%. It was a disappointing quarter as it posted a significant miss of analysts’ EPS estimates.

Icahn Enterprises delivered the weakest performance against analyst estimates and slowest revenue growth in the group. Interestingly, the stock is up 2.7% since the results and currently trades at $8.96.

Read our full analysis of Icahn Enterprises’s results here.

Crane (NYSE: CR)

Based in Connecticut, Crane (NYSE: CR) is a diversified manufacturer of engineered industrial products, including fluid handling, and aerospace technologies.

Crane reported revenues of $557.6 million, up 9.3% year on year. This print topped analysts’ expectations by 1.5%. Overall, it was a strong quarter as it also produced a solid beat of analysts’ organic revenue estimates and a decent beat of analysts’ EPS estimates.

The stock is up 19.8% since reporting and currently trades at $177.94.

Read our full, actionable report on Crane here, it’s free.

Illinois Tool Works (NYSE: ITW)

Founded by Byron Smith, an investor who held over 100 patents, Illinois Tool Works (NYSE: ITW) manufactures engineered components and specialized equipment for numerous industries.

Illinois Tool Works reported revenues of $3.84 billion, down 3.4% year on year. This number was in line with analysts’ expectations. Zooming out, it was a slower quarter as it logged a miss of analysts’ adjusted operating income estimates.

The stock is up 4.3% since reporting and currently trades at $252.20.

Read our full, actionable report on Illinois Tool Works here, it’s free.

Market Update

The Fed’s interest rate hikes throughout 2022 and 2023 have successfully cooled post-pandemic inflation, bringing it closer to the 2% target. Inflationary pressures have eased without tipping the economy into a recession, suggesting a soft landing. This stability, paired with recent rate cuts (0.5% in September 2024 and 0.25% in November 2024), fueled a strong year for the stock market in 2024. The markets surged further after Donald Trump’s presidential victory in November, with major indices reaching record highs in the days following the election. Still, questions remain about the direction of economic policy, as potential tariffs and corporate tax changes add uncertainty for 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.