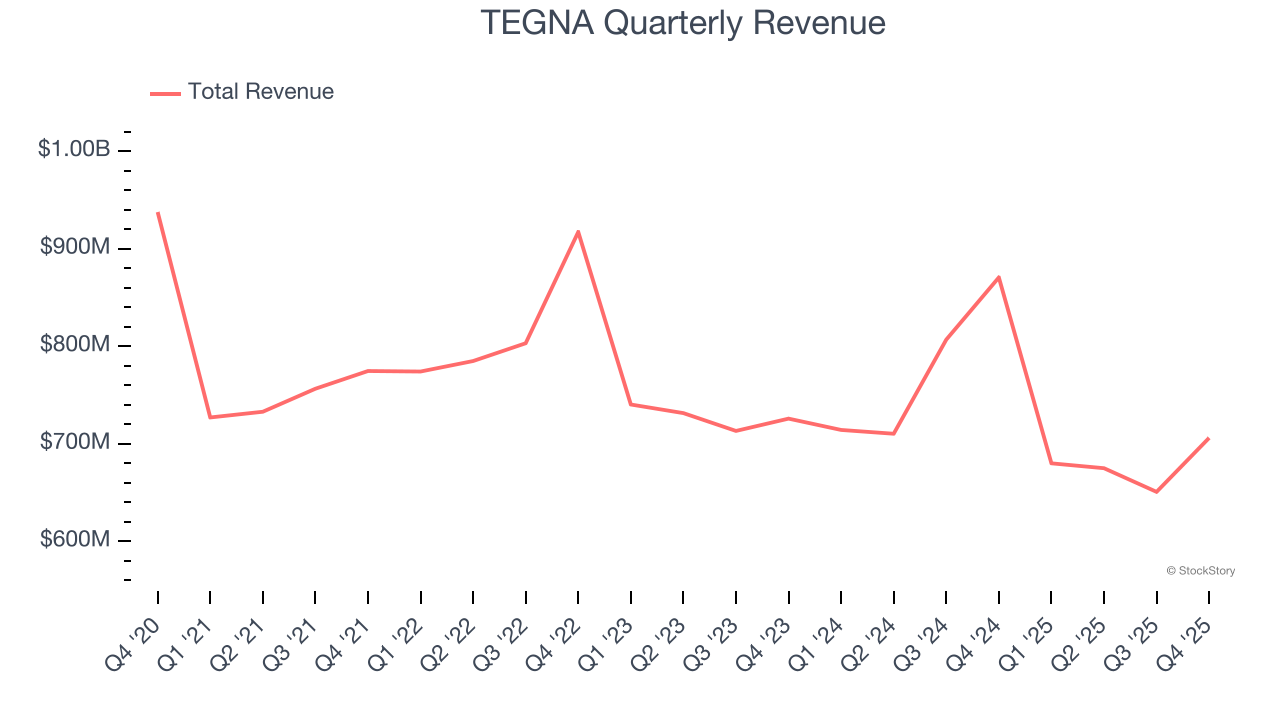

Broadcasting and digital media company TEGNA (NYSE: TGNA) reported Q4 CY2025 results exceeding the market’s revenue expectations, but sales fell by 18.9% year on year to $706.1 million. Its non-GAAP profit of $0.50 per share was 10.6% above analysts’ consensus estimates.

Is now the time to buy TEGNA? Find out by accessing our full research report, it’s free.

TEGNA (TGNA) Q4 CY2025 Highlights:

- Revenue: $706.1 million vs analyst estimates of $699.1 million (18.9% year-on-year decline, 1% beat)

- Adjusted EPS: $0.50 vs analyst estimates of $0.45 (10.6% beat)

- Adjusted EBITDA: $161.1 million vs analyst estimates of $155 million (22.8% margin, 3.9% beat)

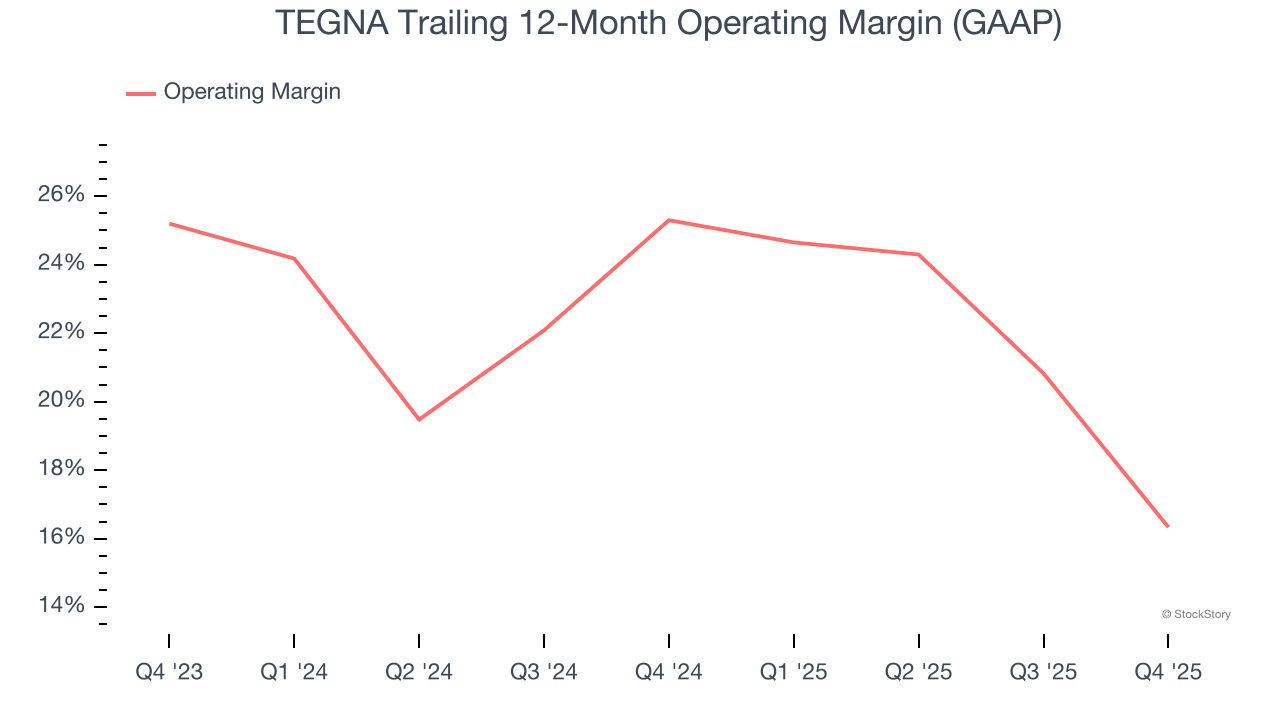

- Operating Margin: 16.9%, down from 31.6% in the same quarter last year

- Free Cash Flow Margin: 12.3%, down from 26.8% in the same quarter last year

- Market Capitalization: $3.37 billion

Company Overview

Spun out of Gannett in 2015, TEGNA (NYSE: TGNA) is a media company operating a network of television stations and digital platforms, focusing on local news and community content.

Revenue Growth

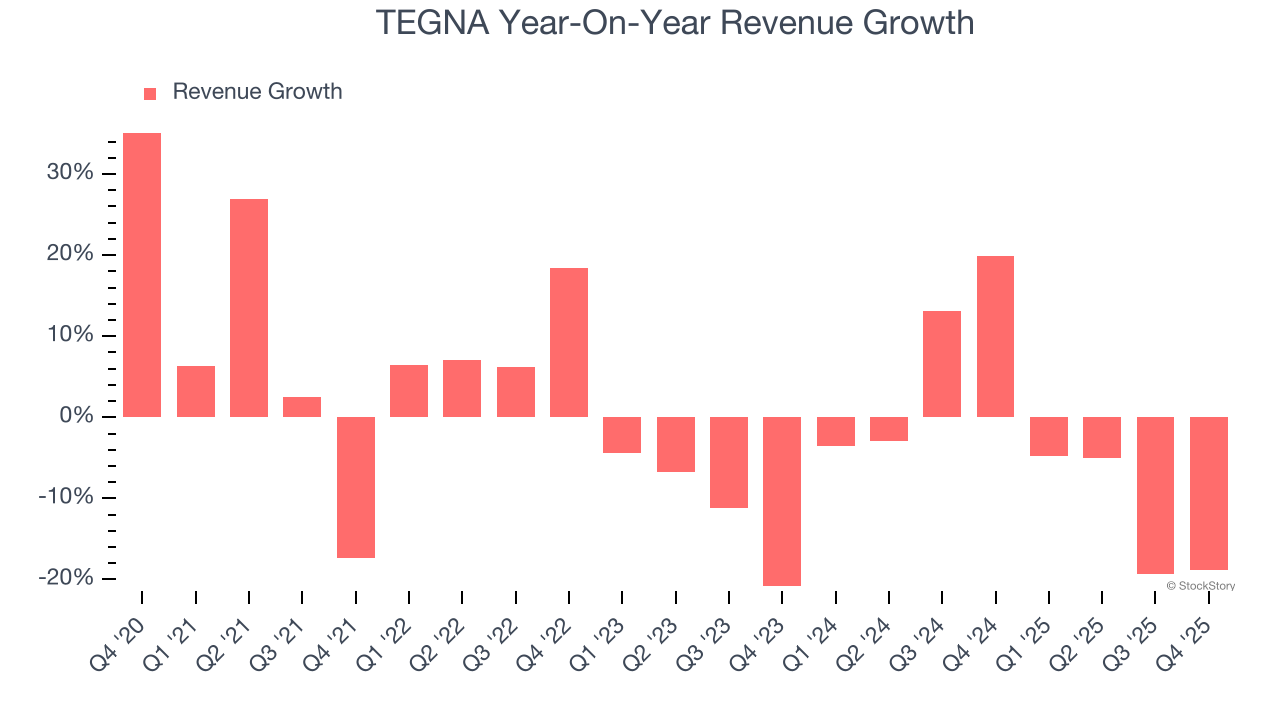

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, TEGNA’s demand was weak and its revenue declined by 1.6% per year. This was below our standards and suggests it’s a low quality business.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. TEGNA’s recent performance shows its demand remained suppressed as its revenue has declined by 3.5% annually over the last two years.

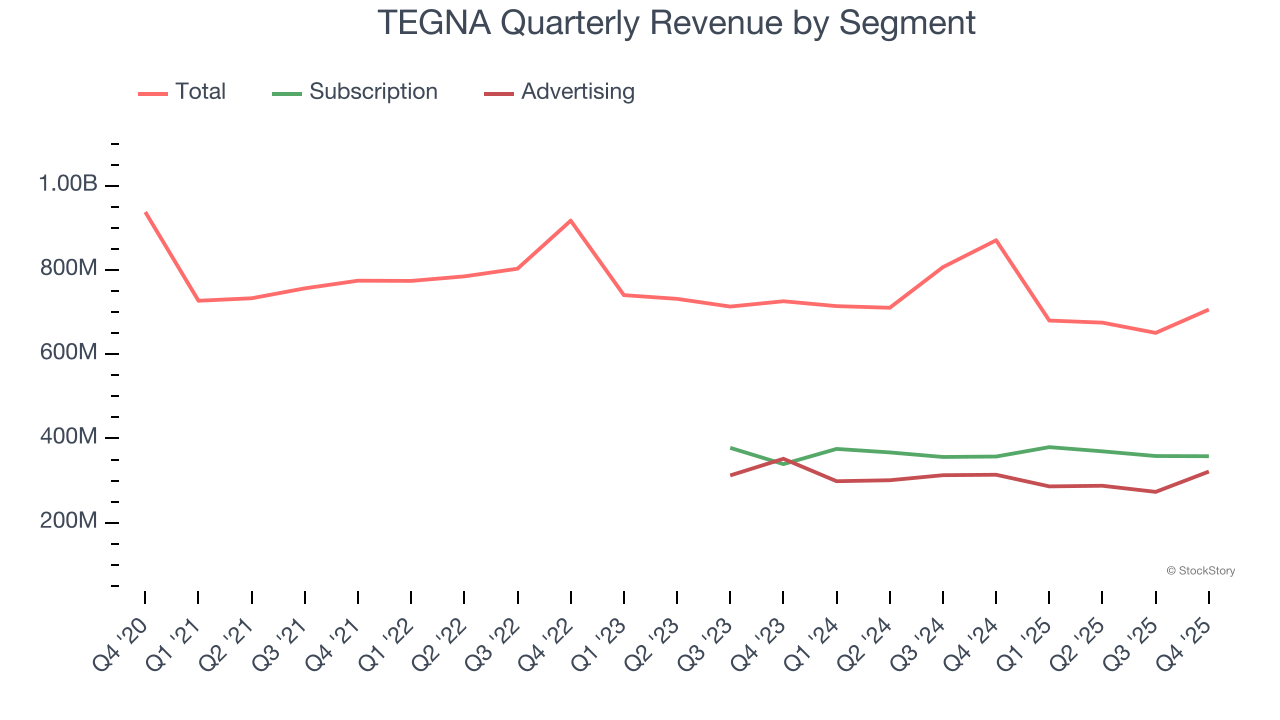

TEGNA also breaks out the revenue for its most important segments, Subscription and Advertising, which are 50.7% and 45.5% of revenue. Over the last two years, TEGNA’s Subscription revenue (access to content) was flat while its Advertising revenue (marketing services) averaged 4.9% year-on-year declines.

This quarter, TEGNA’s revenue fell by 18.9% year on year to $706.1 million but beat Wall Street’s estimates by 1%.

Looking ahead, sell-side analysts expect revenue to grow 10.9% over the next 12 months. Although this projection suggests its newer products and services will catalyze better top-line performance, it is still below the sector average.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

TEGNA’s operating margin has shrunk over the last 12 months and averaged 21.1% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

This quarter, TEGNA generated an operating margin profit margin of 16.9%, down 14.7 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

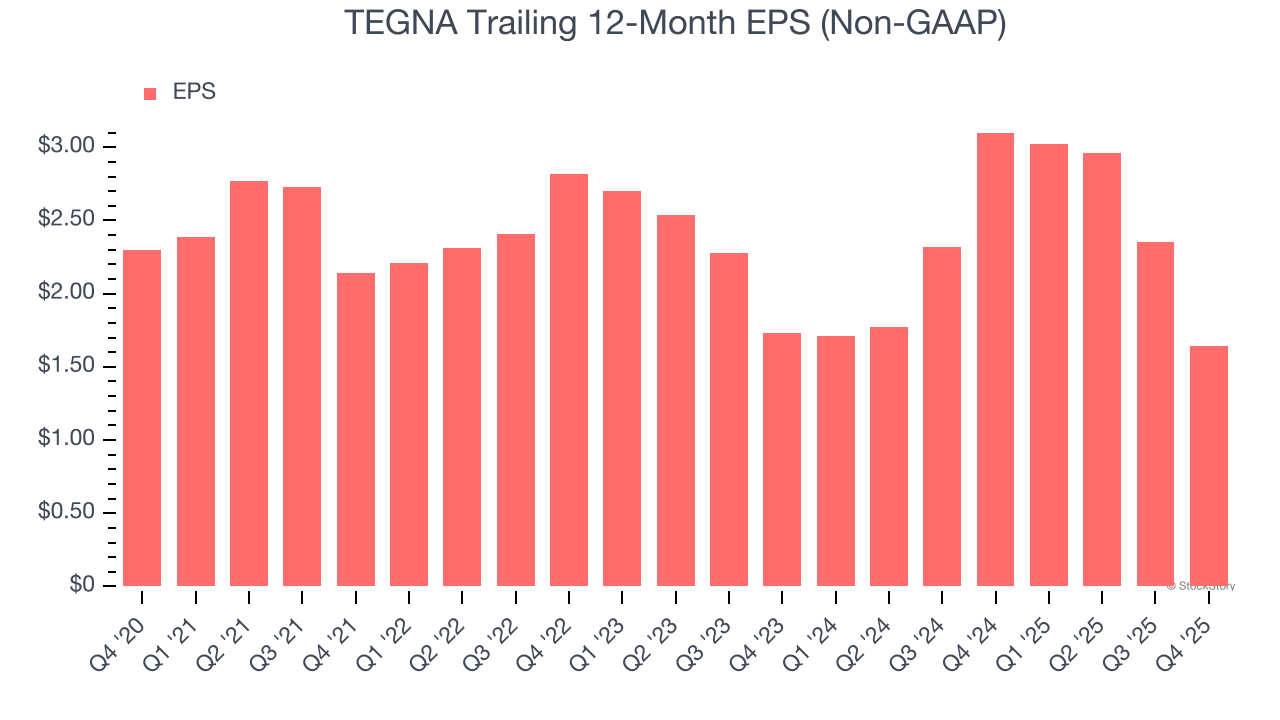

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for TEGNA, its EPS declined by 6.5% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

In Q4, TEGNA reported adjusted EPS of $0.50, down from $1.21 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects TEGNA’s full-year EPS of $1.64 to grow 87.6%.

Key Takeaways from TEGNA’s Q4 Results

It was good to see TEGNA beat analysts’ EPS expectations this quarter. We were also happy its EBITDA outperformed Wall Street’s estimates. Overall, this print had some key positives. The stock remained flat at $20.87 immediately following the results.

Should you buy the stock or not? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).