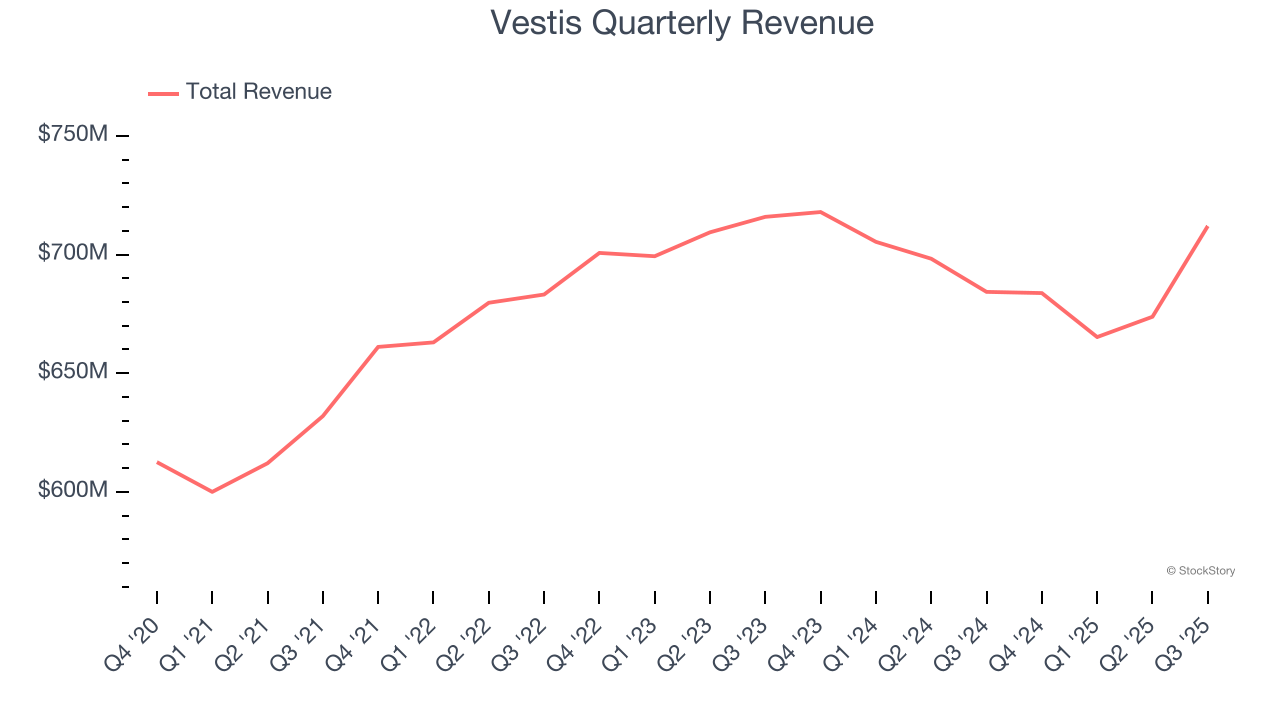

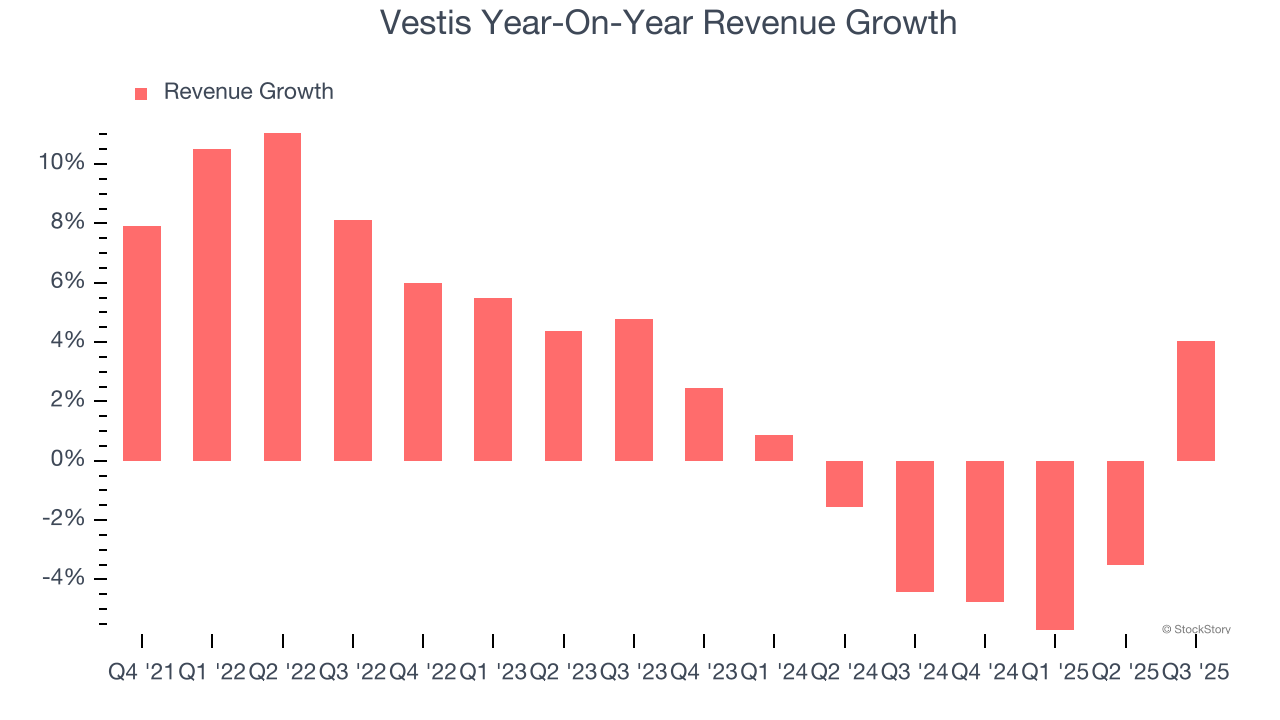

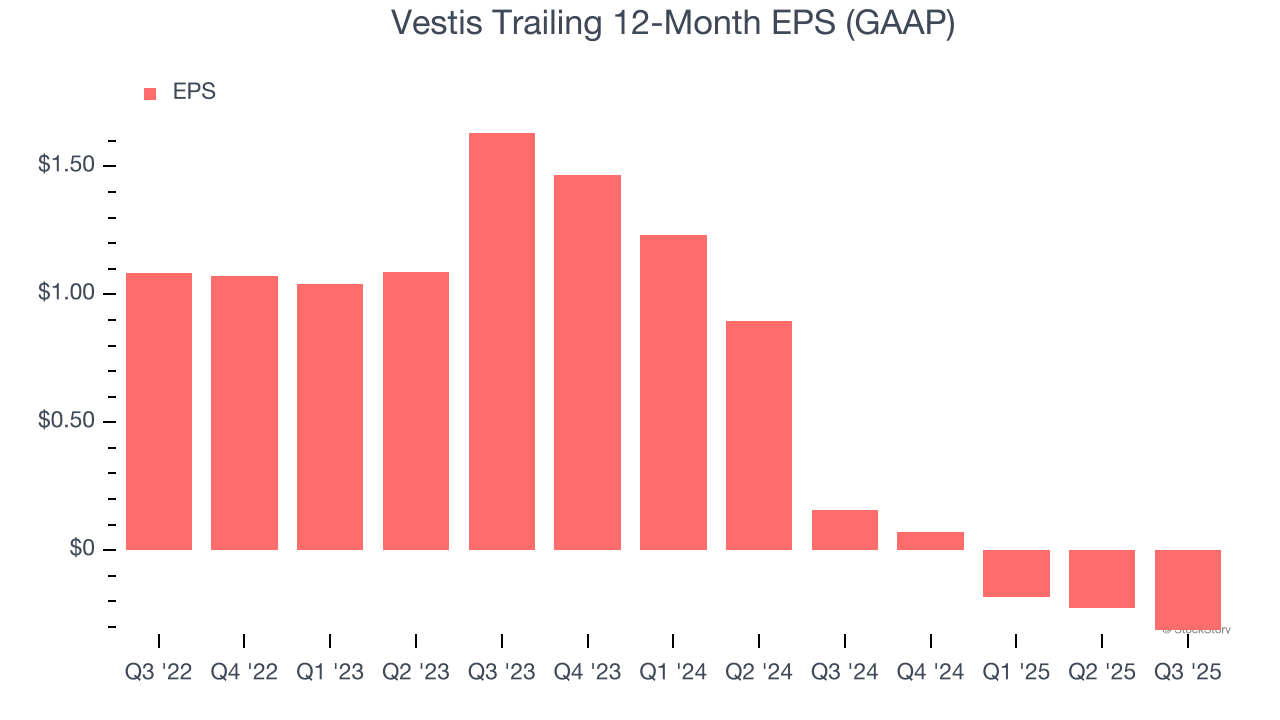

Uniform rental provider Vestis Corporation (NYSE: VSTS) announced better-than-expected revenue in Q3 CY2025, with sales up 4.1% year on year to $712 million. Its GAAP loss of $0.10 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Vestis? Find out by accessing our full research report, it’s free for active Edge members.

Vestis (VSTS) Q3 CY2025 Highlights:

- Revenue: $712 million vs analyst estimates of $685.5 million (4.1% year-on-year growth, 3.9% beat)

- EPS (GAAP): -$0.10 vs analyst estimates of -$0.02 (significant miss)

- Adjusted EBITDA: $64.66 million vs analyst estimates of $67.4 million (9.1% margin, 4.1% miss)

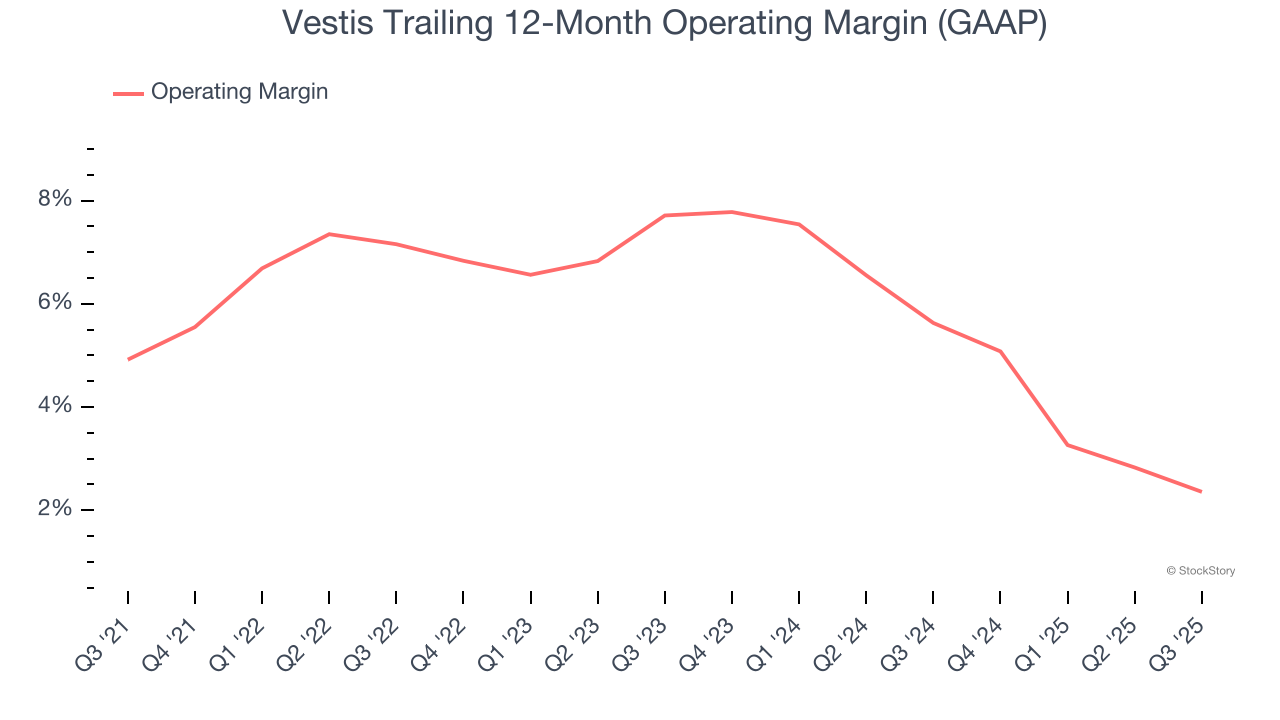

- Operating Margin: 2.5%, down from 4.4% in the same quarter last year

- Free Cash Flow Margin: 2.2%, down from 5.8% in the same quarter last year

- Market Capitalization: $854.3 million

“We ended fiscal 2025 in a good position to advance our strategic priorities as we enter fiscal 2026,” said Jim Barber, President and CEO.

Company Overview

Operating a network of more than 350 facilities with 3,300 delivery routes serving customers weekly, Vestis (NYSE: VSTS) provides uniform rentals, workplace supplies, and facility services to over 300,000 business locations across the United States and Canada.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $2.73 billion in revenue over the past 12 months, Vestis is a mid-sized business services company, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

As you can see below, Vestis’s 2.7% annualized revenue growth over the last four years was sluggish. This shows it failed to generate demand in any major way and is a rough starting point for our analysis.

Long-term growth is the most important, but within business services, a stretched historical view may miss new innovations or demand cycles. Vestis’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 1.6% annually.

This quarter, Vestis reported modest year-on-year revenue growth of 4.1% but beat Wall Street’s estimates by 3.9%.

Looking ahead, sell-side analysts expect revenue to decline by 1.4% over the next 12 months, similar to its two-year rate. This projection is underwhelming and implies its newer products and services will not lead to better top-line performance yet.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

Vestis was profitable over the last five years but held back by its large cost base. Its average operating margin of 5.6% was weak for a business services business.

Analyzing the trend in its profitability, Vestis’s operating margin decreased by 2.6 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Vestis’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, Vestis generated an operating margin profit margin of 2.5%, down 1.9 percentage points year on year. This reduction is quite minuscule and indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Vestis, its EPS declined by more than its revenue over the last two years, dropping 48%. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

We can take a deeper look into Vestis’s earnings to better understand the drivers of its performance. Vestis’s operating margin has declined over the last two years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q3, Vestis reported EPS of negative $0.10, down from negative $0.02 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast Vestis’s full-year EPS of negative $0.31 will flip to positive $0.09.

Key Takeaways from Vestis’s Q3 Results

We enjoyed seeing Vestis beat analysts’ revenue expectations this quarter. On the other hand, its EPS missed. Overall, this was a softer quarter. The stock traded down 5.2% to $6.37 immediately after reporting.

Vestis may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.