Constellation Brands has gotten torched over the last six months - since August 2024, its stock price has dropped 32.4% to $162.99 per share. This was partly due to its softer quarterly results and may have investors wondering how to approach the situation.

Is there a buying opportunity in Constellation Brands, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Even though the stock has become cheaper, we're cautious about Constellation Brands. Here are three reasons why STZ doesn't excite us and a stock we'd rather own.

Why Is Constellation Brands Not Exciting?

With a presence in more than 100 countries, Constellation Brands (NYSE: STZ) is a globally renowned producer and marketer of beer, wine, and spirits.

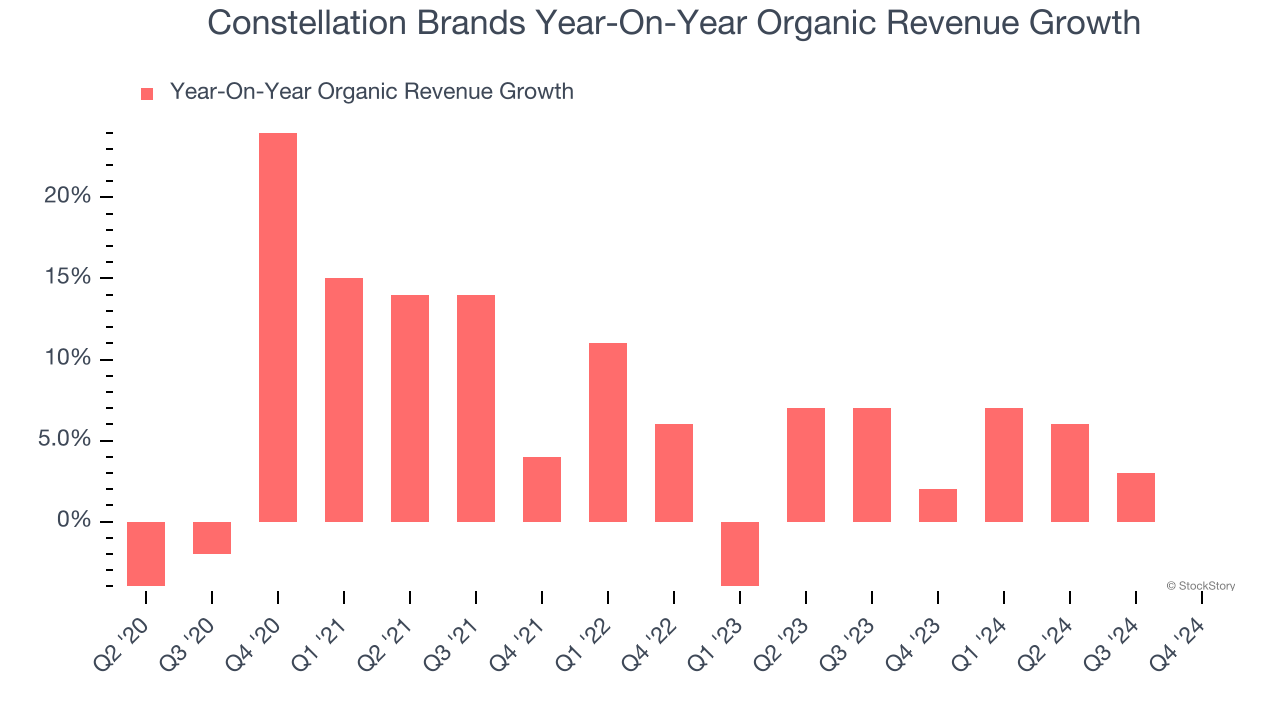

1. Slow Organic Growth Suggests Waning Demand In Core Business

When analyzing revenue growth, we care most about organic revenue growth. This metric captures a business’s performance excluding one-time events such as mergers, acquisitions, and divestitures as well as foreign currency fluctuations.

The demand for Constellation Brands’s products has generally risen over the last two years but lagged behind the broader sector. On average, the company’s organic sales have grown by 3.5% year on year.

2. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Constellation Brands’s revenue to rise by 3%, a slight deceleration versus its 5.5% annualized growth for the past three years. This projection doesn't excite us and implies its products will face some demand challenges.

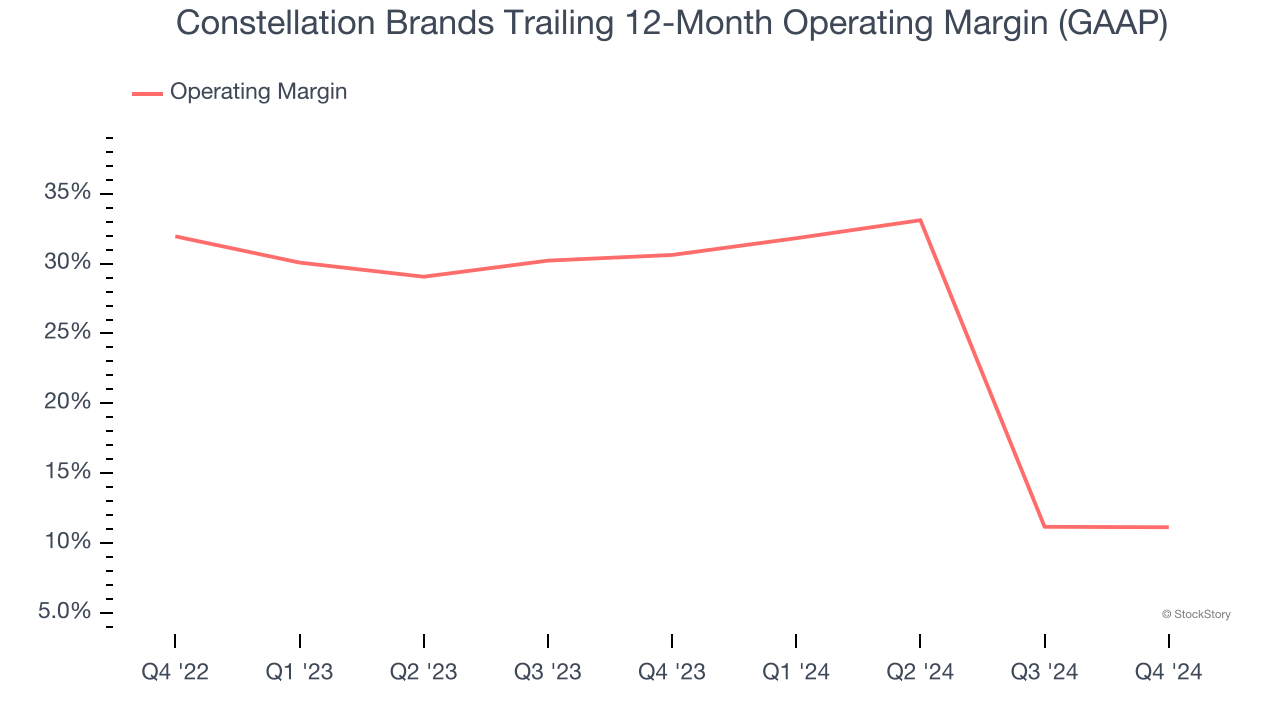

3. Operating Margin Falling

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Looking at the trend in its profitability, Constellation Brands’s operating margin decreased by 19.5 percentage points over the last year. Even though its historical margin is high, shareholders will want to see Constellation Brands become more profitable in the future. Its operating margin for the trailing 12 months was 11.1%.

Final Judgment

Constellation Brands’s business quality ultimately falls short of our standards. Following the recent decline, the stock trades at 11× forward price-to-earnings (or $162.99 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere. We’d recommend looking at the most entrenched endpoint security platform on the market.

Stocks We Would Buy Instead of Constellation Brands

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.