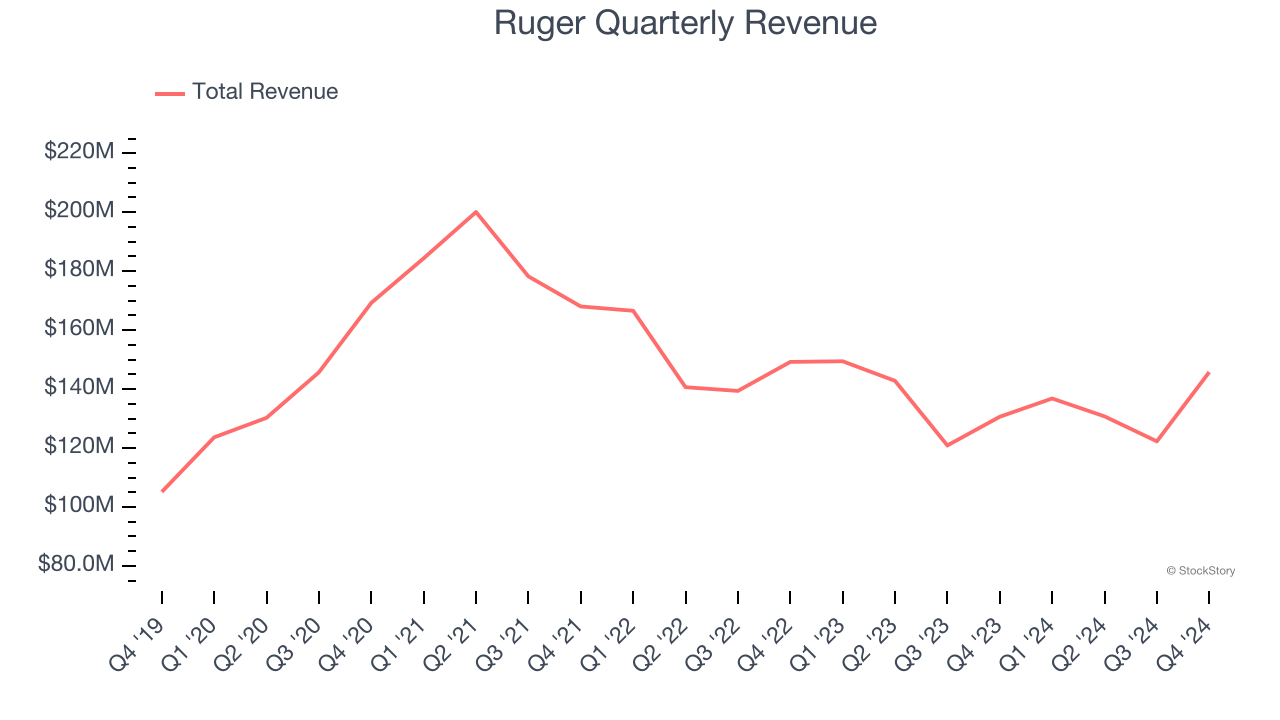

American firearm manufacturing company Ruger (NYSE: RGR) reported Q4 CY2024 results beating Wall Street’s revenue expectations, with sales up 11.6% year on year to $145.8 million. Its GAAP profit of $0.61 per share increased from $0.58 in the same quarter last year.

Is now the time to buy Ruger? Find out by accessing our full research report, it’s free.

Ruger (RGR) Q4 CY2024 Highlights:

- Revenue: $145.8 million vs analyst estimates of $137.8 million (11.6% year-on-year growth, 5.8% beat)

- Adjusted EBITDA: $17.63 million vs analyst estimates of $18.43 million (12.1% margin, 4.4% miss)

- Operating Margin: 7.8%, in line with the same quarter last year

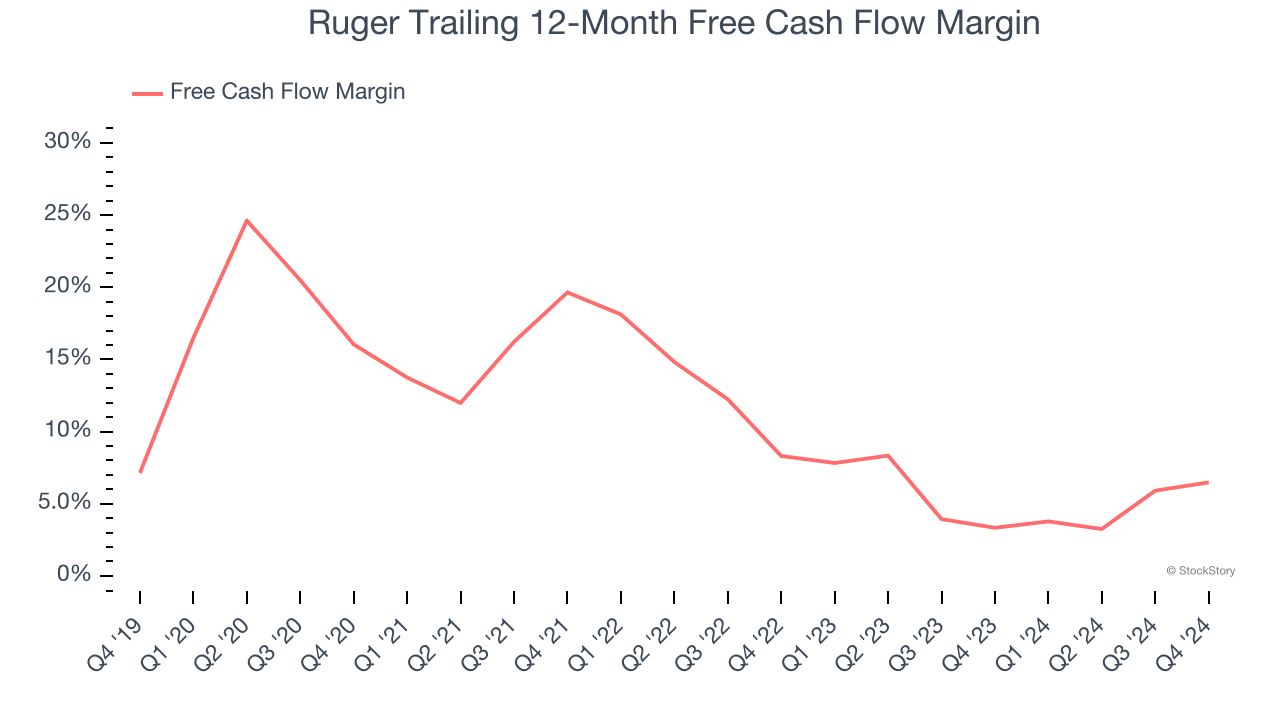

- Free Cash Flow Margin: 11.2%, up from 9.5% in the same quarter last year

- Market Capitalization: $602 million

Chief Executive Officer Christopher J. Killoy commented on the Company’s strong finish to the year, “We were pleased with our sales growth and improved profitability in the fourth quarter, despite the apparent reduction in consumer demand, as adjusted NICS checks decreased 6% from the prior year. Our disciplined approach, long-term focus on generating shareholder value, diverse product catalog, and commitment to new product development allow us to succeed during the ebbs and flows of the firearms market. We enter 2025 with a strong, debt-free balance sheet, reduced inventories at our independent distributors, and a full pipeline of recently launched new products and many others still under development.”

Company Overview

Founded in 1949, Ruger (NYSE: RGR) is an American manufacturer of firearms for the commercial sporting market.

Leisure Products

Leisure products cover a wide range of goods in the consumer discretionary sector. Maintaining a strong brand is key to success, and those who differentiate themselves will enjoy customer loyalty and pricing power while those who don’t may find themselves in precarious positions due to the non-essential nature of their offerings.

Sales Growth

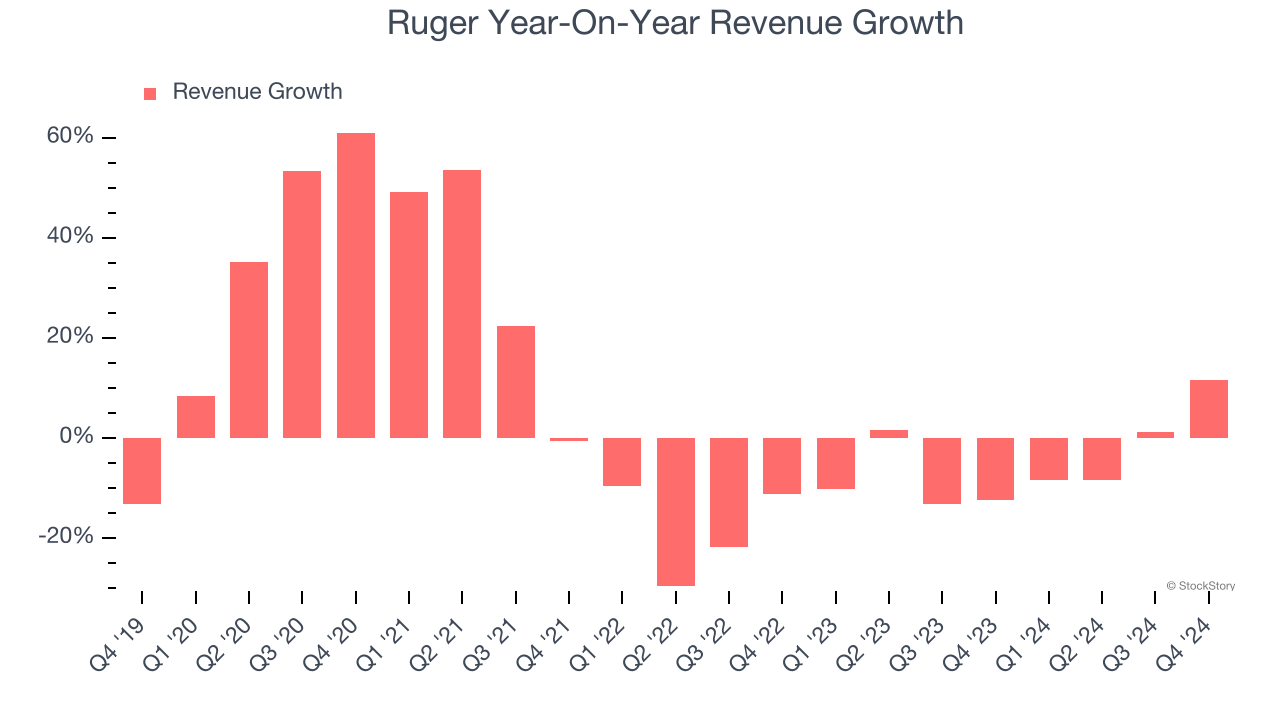

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Regrettably, Ruger’s sales grew at a sluggish 5.5% compounded annual growth rate over the last five years. This fell short of our benchmark for the consumer discretionary sector and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Ruger’s history shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 5.2% annually.

This quarter, Ruger reported year-on-year revenue growth of 11.6%, and its $145.8 million of revenue exceeded Wall Street’s estimates by 5.8%.

Looking ahead, sell-side analysts expect revenue to grow 3.2% over the next 12 months. Although this projection suggests its newer products and services will fuel better top-line performance, it is still below the sector average.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Ruger has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 4.9%, lousy for a consumer discretionary business.

Ruger’s free cash flow clocked in at $16.4 million in Q4, equivalent to a 11.2% margin. This result was good as its margin was 1.7 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends trump fluctuations.

Key Takeaways from Ruger’s Q4 Results

We enjoyed seeing Ruger exceed analysts’ revenue expectations this quarter. The stock traded up 2.3% to $36.30 immediately after reporting.

Ruger put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.