Enviri’s stock price has taken a beating over the past six months, shedding 36.6% of its value and falling to $6.59 per share. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in Enviri, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Even with the cheaper entry price, we don't have much confidence in Enviri. Here are three reasons why there are better opportunities than NVRI and a stock we'd rather own.

Why Do We Think Enviri Will Underperform?

Cooling America’s first indoor ice rink in the 19th century, Enviri (NYSE: NVRI) offers steel and waste handling services.

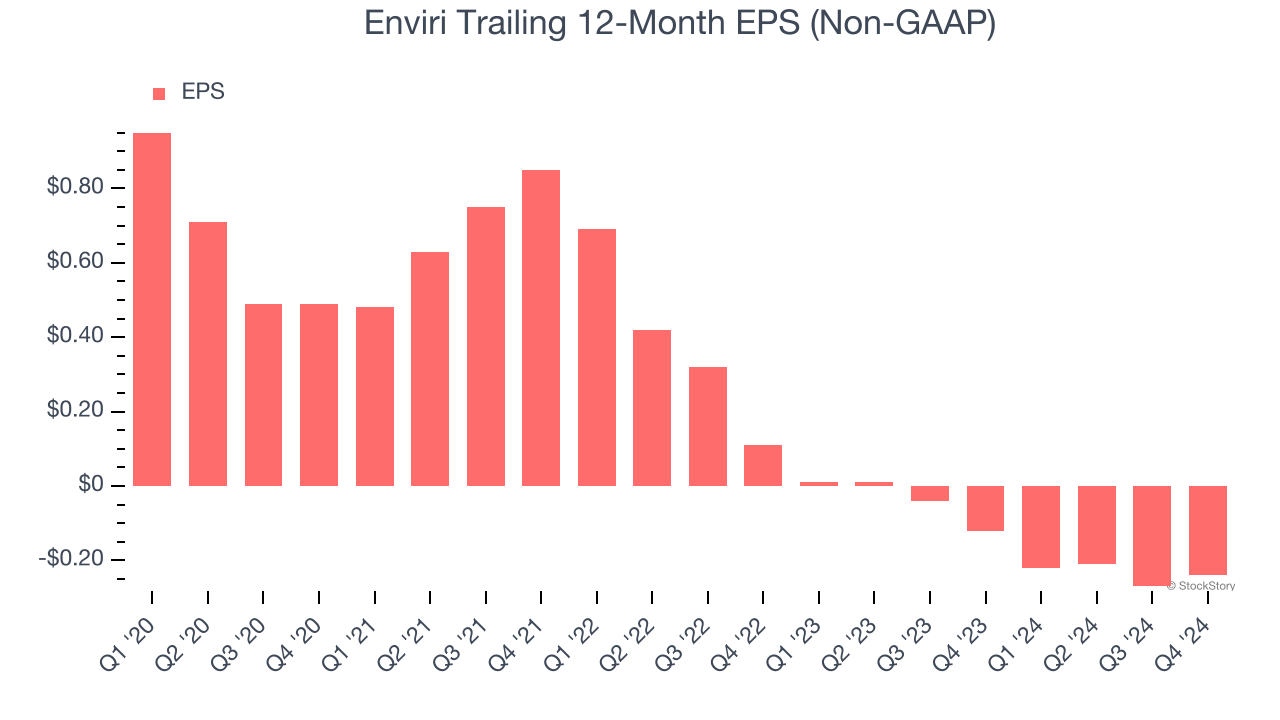

1. EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Enviri, its EPS declined by 15.3% annually over the last five years while its revenue grew by 9.3%. This tells us the company became less profitable on a per-share basis as it expanded.

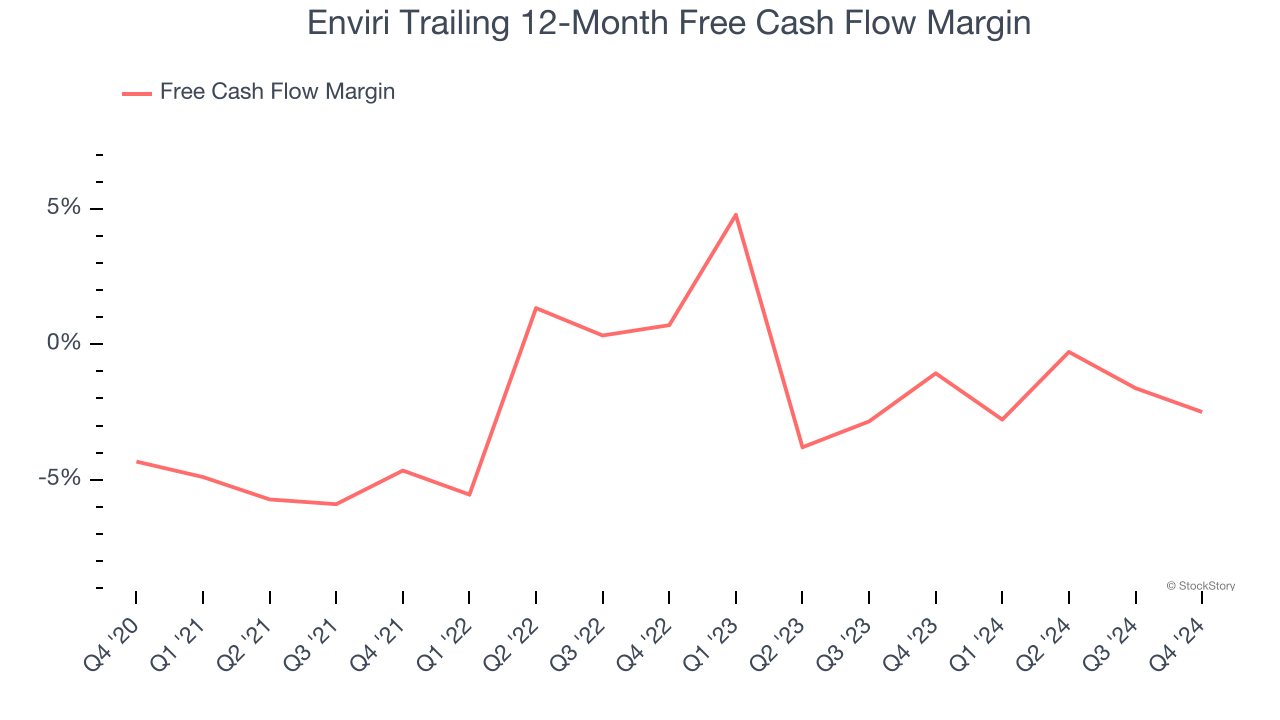

2. Cash Burn Ignites Concerns

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

While Enviri’s free cash flow broke even this quarter, the broader story hasn’t been so clean. Enviri’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 2.2%, meaning it lit $2.24 of cash on fire for every $100 in revenue.

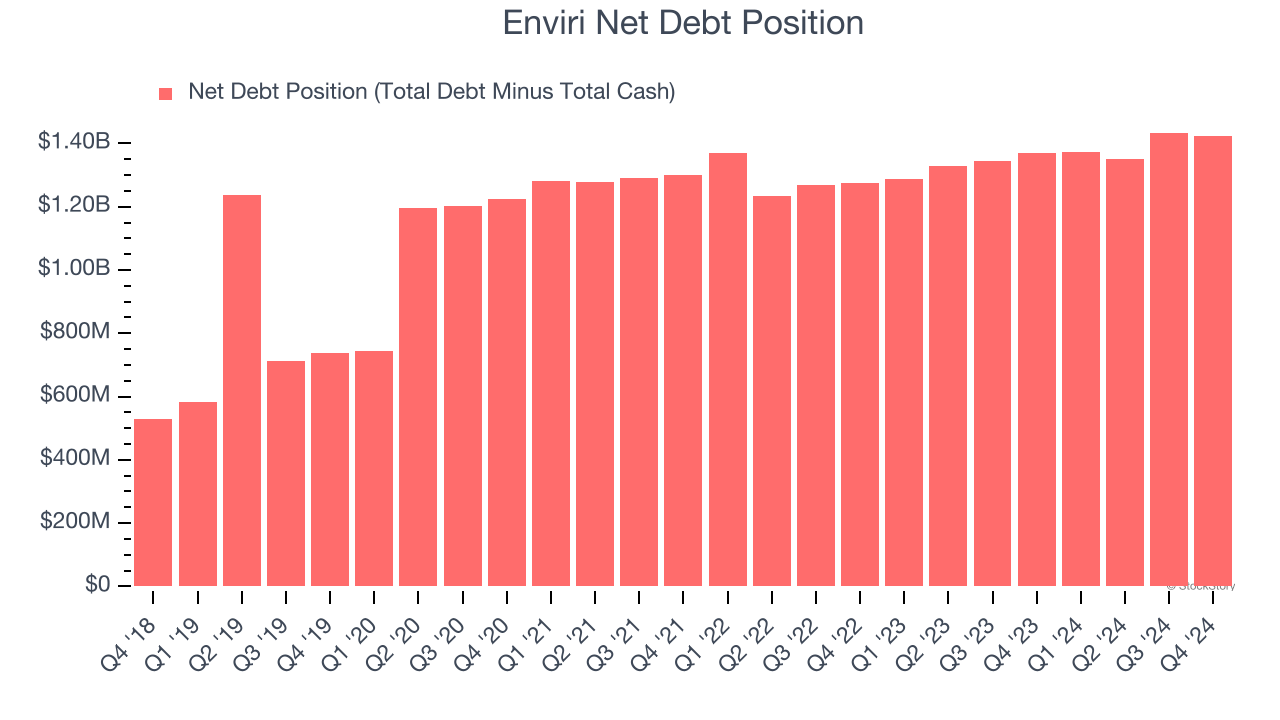

3. Short Cash Runway Exposes Shareholders to Potential Dilution

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Enviri burned through $58.53 million of cash over the last year, and its $1.51 billion of debt exceeds the $88.36 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

Unless the Enviri’s fundamentals change quickly, it might find itself in a position where it must raise capital from investors to continue operating. Whether that would be favorable is unclear because dilution is a headwind for shareholder returns.

We remain cautious of Enviri until it generates consistent free cash flow or any of its announced financing plans materialize on its balance sheet.

Final Judgment

Enviri falls short of our quality standards. Following the recent decline, the stock trades at 63.4× forward price-to-earnings (or $6.59 per share). At this valuation, there’s a lot of good news priced in - we think there are better investment opportunities out there. Let us point you toward one of our top software and edge computing picks.

Stocks We Would Buy Instead of Enviri

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.