Since October 2024, Yelp has been in a holding pattern, posting a small loss of 3.5% while floating around $33.68.

Given the underwhelming price action, is now a good time to buy YELP? Or should investors expect a bumpy road ahead? Find out in our full research report, it’s free.

Why Does Yelp Spark Debate?

Founded by PayPal alumni Jeremy Stoppelman and Russel Simmons, Yelp (NYSE: YELP) is an online platform that helps people discover local businesses through crowd-sourced reviews.

Two Positive Attributes:

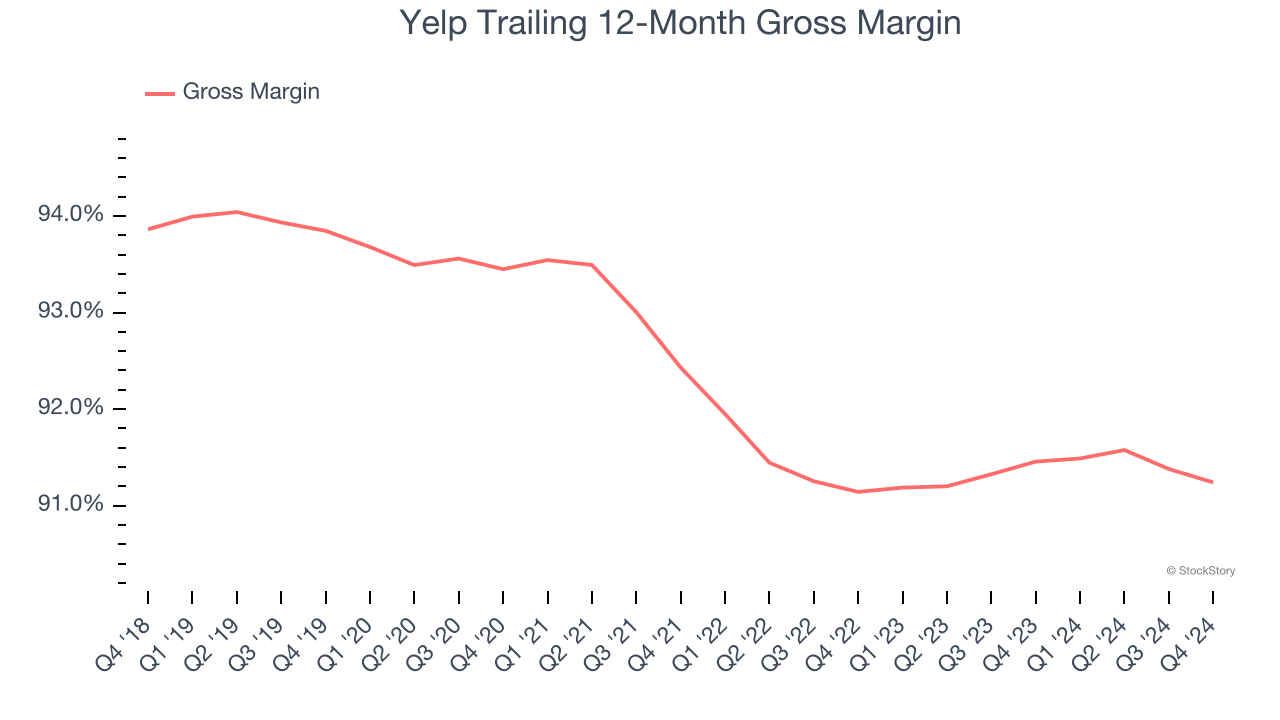

1. Elite Gross Margin Powers Best-In-Class Business Model

A company’s gross profit margin has a significant impact on its ability to exert pricing power, develop new products, and invest in marketing. These factors can determine the winner in a competitive market.

For social network businesses like Yelp, gross profit tells us how much money the company gets to keep after covering the base cost of its products and services, which typically include customer service, data center, and other infrastructure expenses.

Yelp’s gross margin is one of the highest in the consumer internet sector, an output of its asset-lite business model and strong pricing power. It also enables the company to fund large investments in product and marketing during periods of rapid growth to achieve higher profits in the future. As you can see below, it averaged an elite 91.3% gross margin over the last two years. Said differently, roughly $91.35 was left to spend on selling, marketing, and R&D for every $100 in revenue.

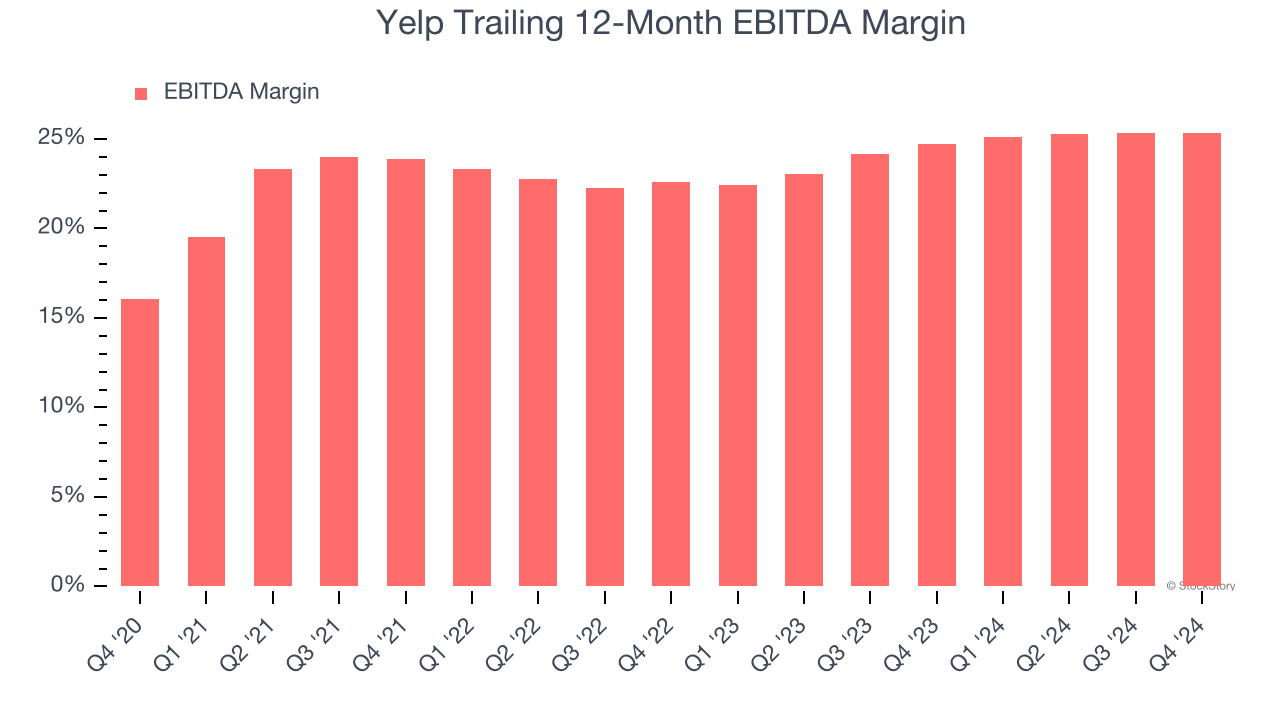

2. EBITDA Margin Reveals a Well-Run Organization

Investors frequently analyze operating income to understand a business’s core profitability. Similar to operating income, EBITDA is a common profitability metric for consumer internet companies because it removes various one-time or non-cash expenses, offering a more normalized view of profit potential.

Yelp has been a well-oiled machine over the last two years. It demonstrated elite profitability for a consumer internet business, boasting an average EBITDA margin of 25%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

One Reason to be Careful:

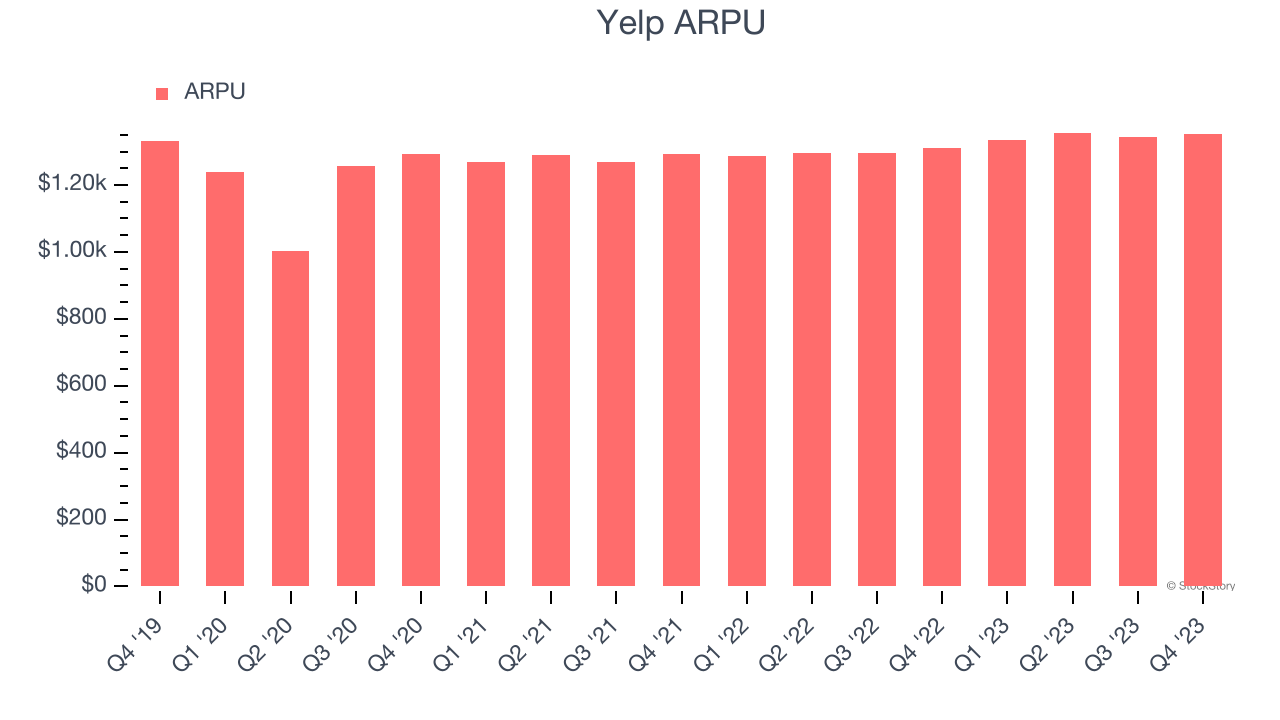

Growth in Customer Spending Lags Peers

Average revenue per user (ARPU) is a critical metric to track because it measures how much the company earns from the ads shown to its users. ARPU can also be a proxy for how valuable advertisers find Yelp’s audience and its ad-targeting capabilities.

Yelp’s ARPU growth has been mediocre over the last two years, averaging 3.9%. This raises questions about its platform’s health and ability to engage its users effectively.

Final Judgment

Yelp’s merits more than compensate for its flaws, but at $33.68 per share (or 6.3× forward EV-to-EBITDA), is now the time to initiate a position? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Yelp

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.