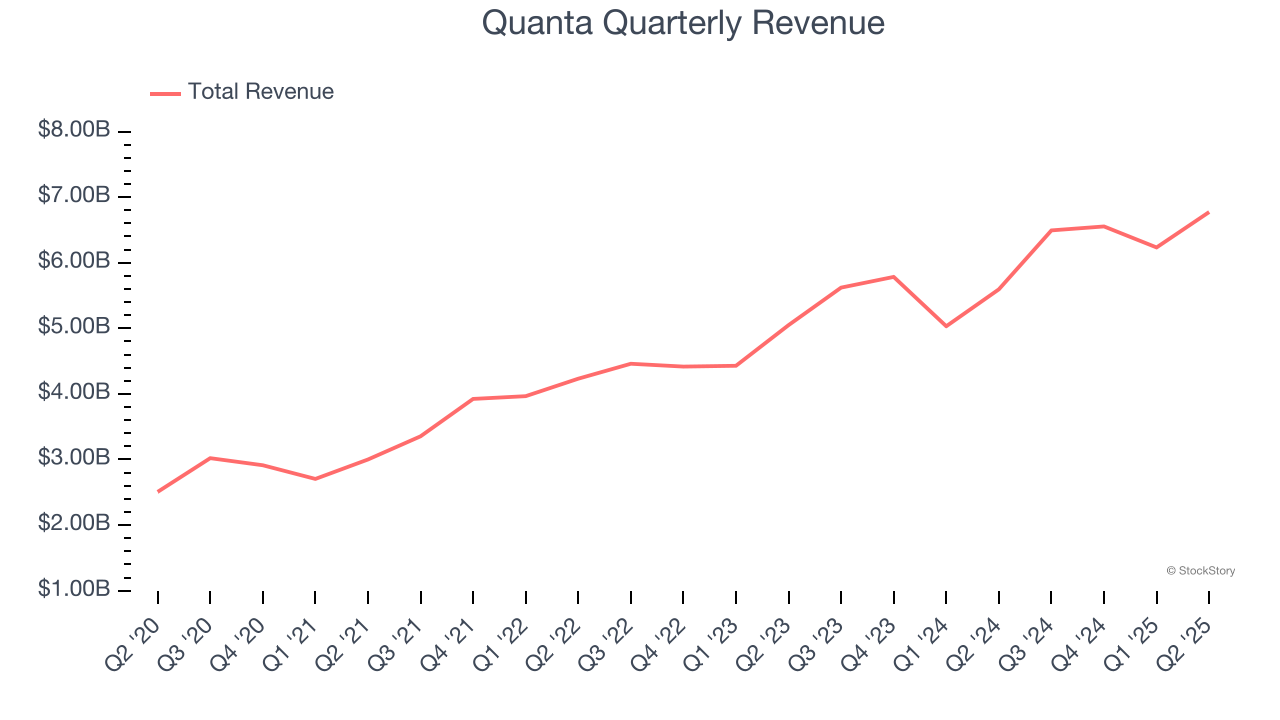

Infrastructure solutions provider Quanta (NYSE: PWR) reported Q2 CY2025 results exceeding the market’s revenue expectations, with sales up 21.1% year on year to $6.77 billion. The company’s full-year revenue guidance of $27.65 billion at the midpoint came in 2.4% above analysts’ estimates. Its non-GAAP profit of $2.48 per share was 1.4% above analysts’ consensus estimates.

Is now the time to buy Quanta? Find out by accessing our full research report, it’s free.

Quanta (PWR) Q2 CY2025 Highlights:

- Revenue: $6.77 billion vs analyst estimates of $6.55 billion (21.1% year-on-year growth, 3.5% beat)

- Adjusted EPS: $2.48 vs analyst estimates of $2.44 (1.4% beat)

- Adjusted EBITDA: $668.8 million vs analyst estimates of $663.5 million (9.9% margin, 0.8% beat)

- The company lifted its revenue guidance for the full year to $27.65 billion at the midpoint from $26.95 billion, a 2.6% increase

- Management raised its full-year Adjusted EPS guidance to $10.58 at the midpoint, a 2.2% increase

- EBITDA guidance for the full year is $2.83 billion at the midpoint, above analyst estimates of $2.74 billion

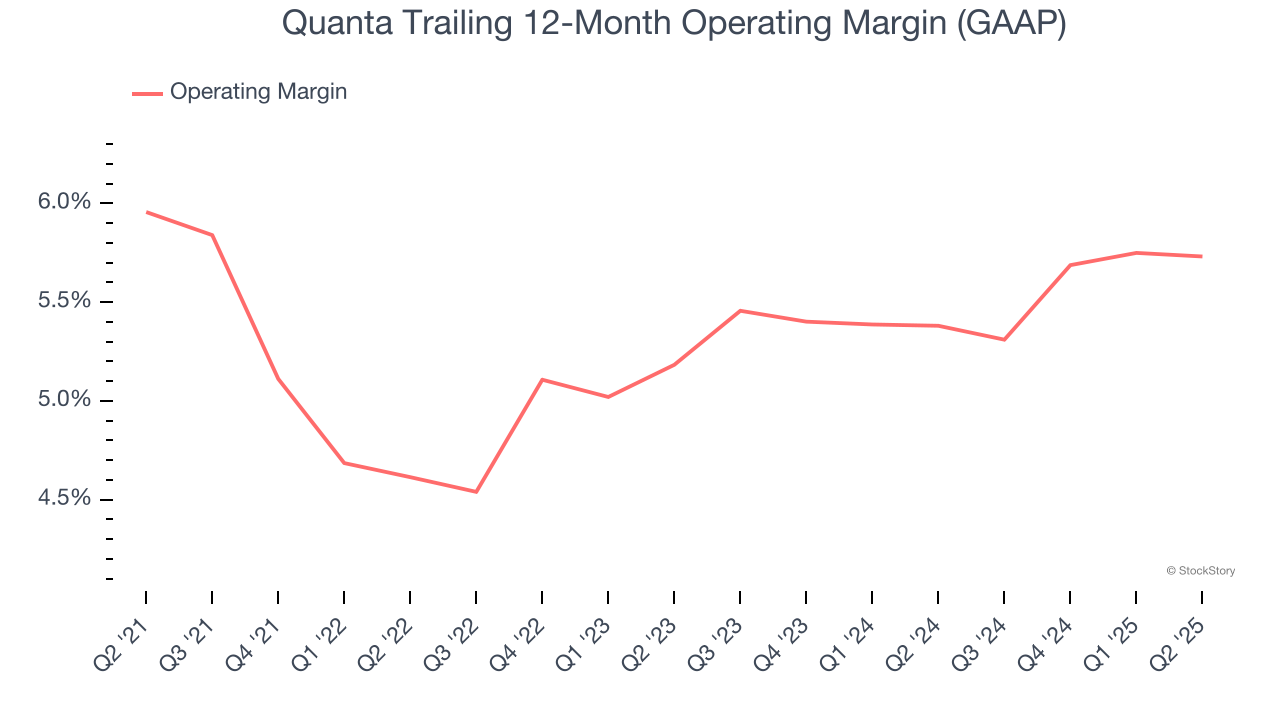

- Operating Margin: 5.5%, in line with the same quarter last year

- Free Cash Flow Margin: 2.3%, down from 4.6% in the same quarter last year

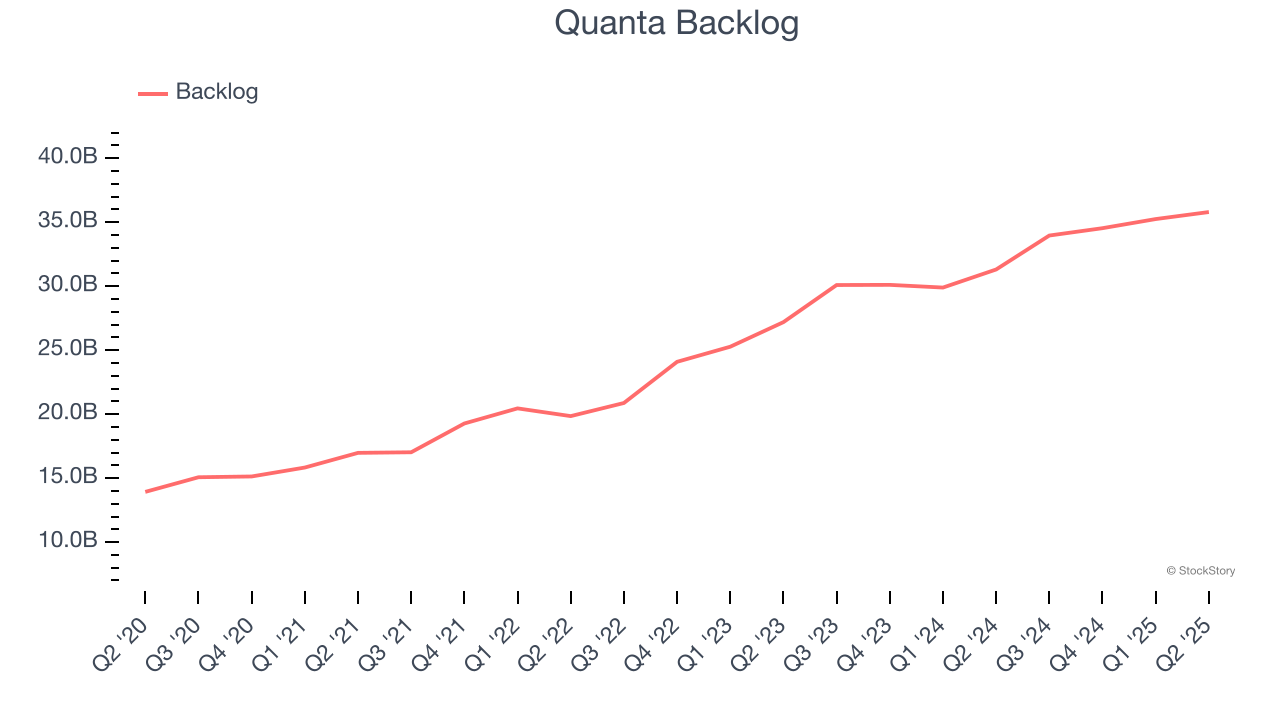

- Backlog: $35.8 billion at quarter end, up 14.3% year on year

- Market Capitalization: $60.93 billion

"Quanta delivered a strong first half of the year, with our second quarter results reflecting another quarter of double-digit growth in revenue, adjusted EBITDA and adjusted earnings per share and record total backlog of $35.8 billion. These results reflect Quanta's ability to provide certainty through the power of our portfolio and world-class execution. Demand for our services remains resilient, fueled by our customers' multi-year programs to build the power grid, generation and energy infrastructure necessary to support load growth from technology adoption and manufacturing reshoring and a focus on reliability and security," said Duke Austin, President and Chief Executive Officer of Quanta Services.

Company Overview

A construction engineering services company, Quanta (NYSE: PWR) provides infrastructure solutions to a variety of sectors, including energy and communications.

Revenue Growth

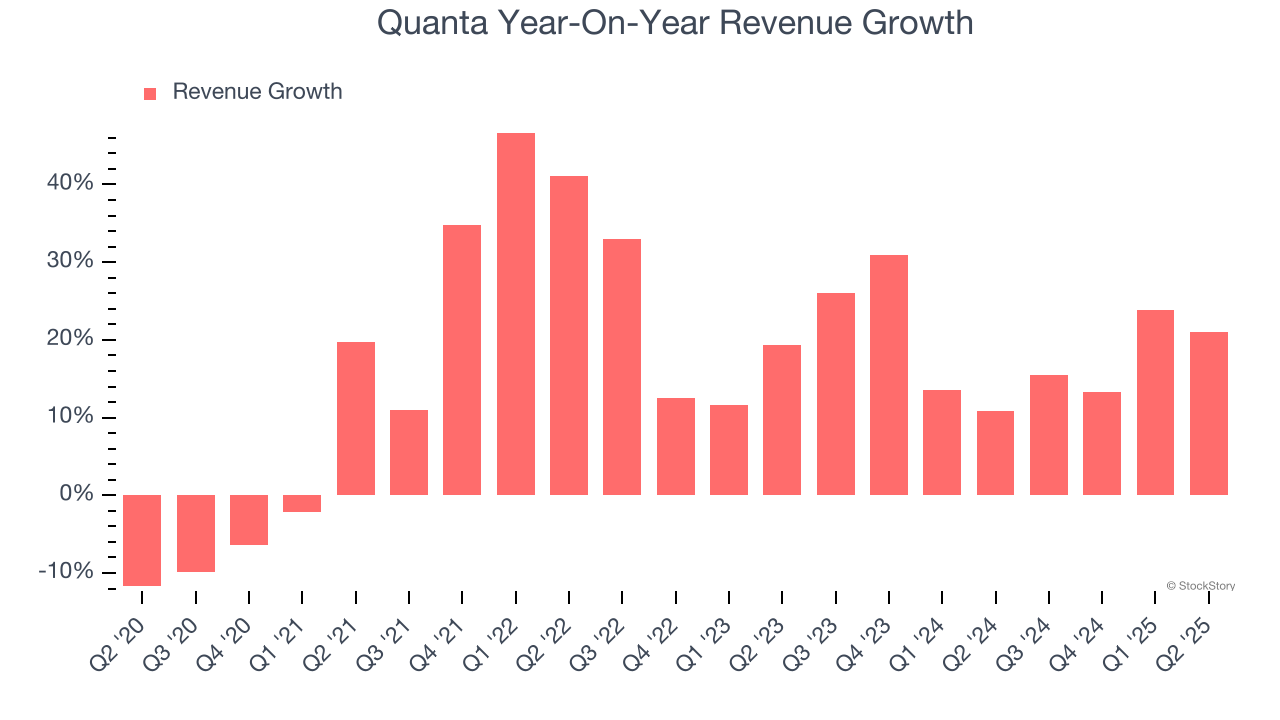

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Quanta grew its sales at an incredible 17.3% compounded annual growth rate. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Quanta’s annualized revenue growth of 19.1% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

We can dig further into the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Quanta’s backlog reached $35.8 billion in the latest quarter and averaged 20.3% year-on-year growth over the last two years. Because this number is in line with its revenue growth, we can see the company effectively balanced its new order intake and fulfillment processes.

This quarter, Quanta reported robust year-on-year revenue growth of 21.1%, and its $6.77 billion of revenue topped Wall Street estimates by 3.5%.

Looking ahead, sell-side analysts expect revenue to grow 8.4% over the next 12 months, a deceleration versus the last two years. We still think its growth trajectory is satisfactory given its scale and suggests the market is baking in success for its products and services.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Quanta’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 5.4% over the last five years. This profitability was paltry for an industrials business and caused by its suboptimal cost structureand low gross margin.

Looking at the trend in its profitability, Quanta’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q2, Quanta generated an operating margin profit margin of 5.5%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

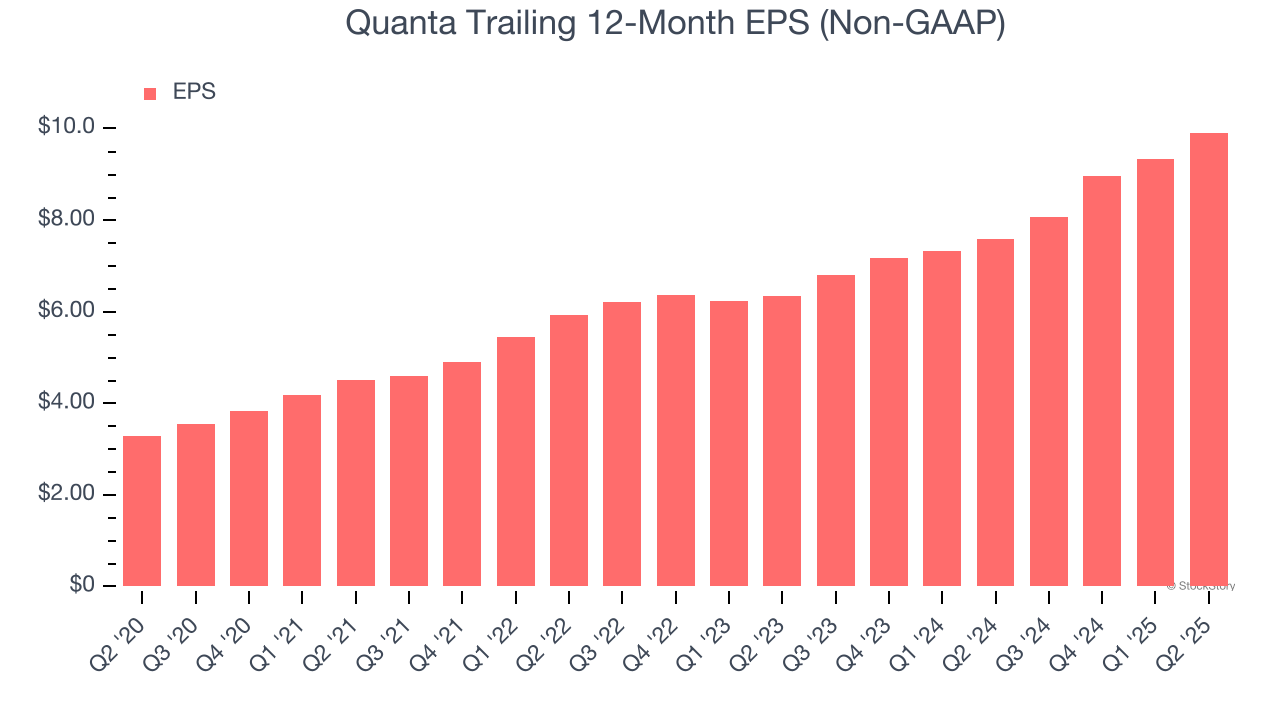

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Quanta’s EPS grew at an astounding 24.8% compounded annual growth rate over the last five years, higher than its 17.3% annualized revenue growth. However, we take this with a grain of salt because its operating margin didn’t improve and it didn’t repurchase its shares, meaning the delta came from reduced interest expenses or taxes.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Quanta, its two-year annual EPS growth of 25.1% is similar to its five-year trend, implying strong and stable earnings power.

In Q2, Quanta reported EPS at $2.48, up from $1.90 in the same quarter last year. This print beat analysts’ estimates by 1.4%. Over the next 12 months, Wall Street expects Quanta’s full-year EPS of $9.92 to grow 12.8%.

Key Takeaways from Quanta’s Q2 Results

This was a beat and raise quarter, with revenue and adjusted EPS coming in ahead of Wall Street's expectations. Looking ahead, the company raised full-year revenue and adjusted EPS guidance, which is usually a promising sign of positive business momentum. On the other hand, its backlog was in line. Overall, we think this was a good quarter with key metrics above expectations. The stock remained flat at $411.10 immediately after reporting.

Is Quanta an attractive investment opportunity at the current price? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.