Live Oak Bancshares has followed the market’s trajectory closely, rising in tandem with the S&P 500 over the past six months. The stock has climbed by 10.1% to $34.35 per share while the index has gained 11.2%.

Is now the time to buy LOB? Find out in our full research report, it’s free for active Edge members.

Why Does LOB Stock Spark Debate?

Founded during the 2008 financial crisis with a vision to reimagine small business banking through technology, Live Oak Bancshares (NYSE: LOB) is a bank holding company that specializes in providing online banking services and SBA-guaranteed loans to small businesses across targeted industries nationwide.

Two Things to Like:

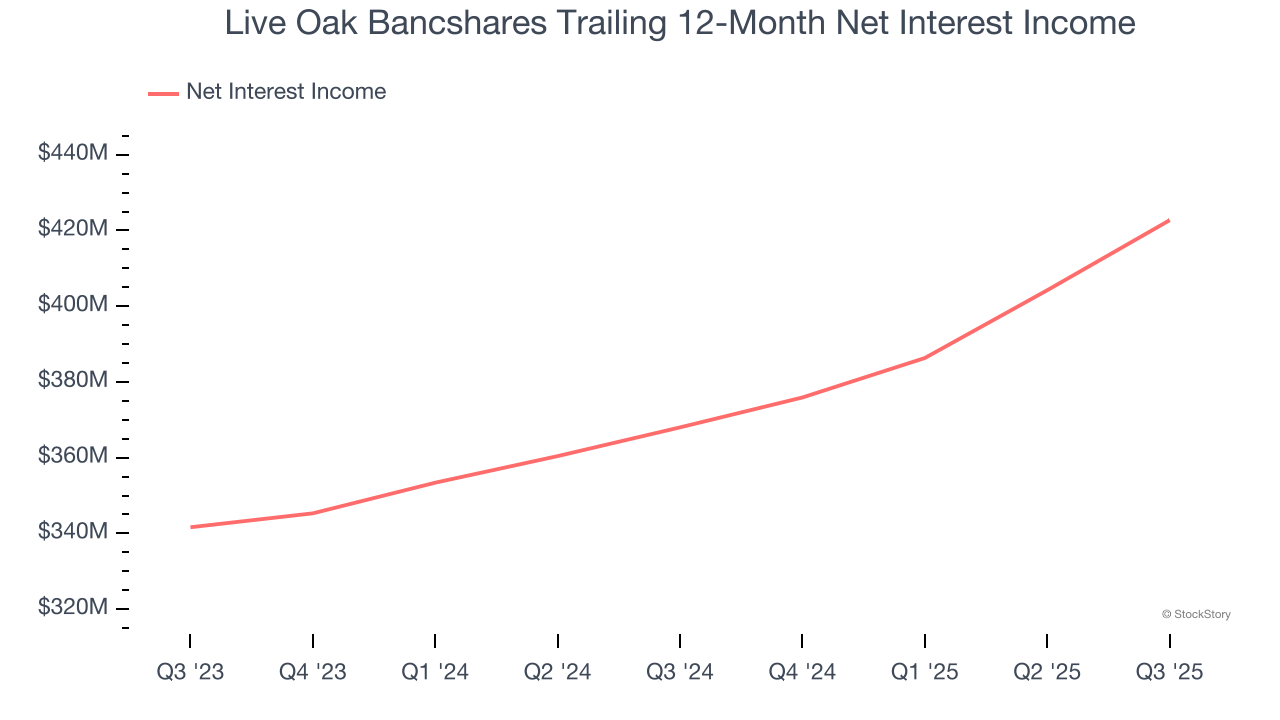

1. Net Interest Income Skyrockets, Fueling Growth Opportunities

Markets consistently prioritize net interest income over non-recurring fees, recognizing its superior quality compared to the more unpredictable revenue streams.

Live Oak Bancshares’s net interest income has grown at a 19.9% annualized rate over the last five years, much better than the broader banking industry and faster than its total revenue. Its growth was driven by both an increase in its outstanding loans and net interest margin, which represents how much a bank earns in relation to its outstanding loan book.

2. Forecasted Efficiency Ratio Shows Stronger Profits Ahead

Topline growth is certainly important, but the overall profitability of this growth matters for the bottom line. For banks, we look at efficiency ratio, which is non-interest expense (salaries, rent, IT, marketing, excluding interest paid out to depositors) as a percentage of total revenue.

Investors place greater emphasis on efficiency ratio movements than absolute values, understanding that expense structures reflect revenue mix variations. Lower ratios represent better operational performance since they show banks generating more revenue per dollar of expense.

For the next 12 months, Wall Street expects Live Oak Bancshares to rein in some of its expenses as it anticipates an efficiency ratio of 57.2% compared to 62.4% over the past year.

One Reason to be Careful:

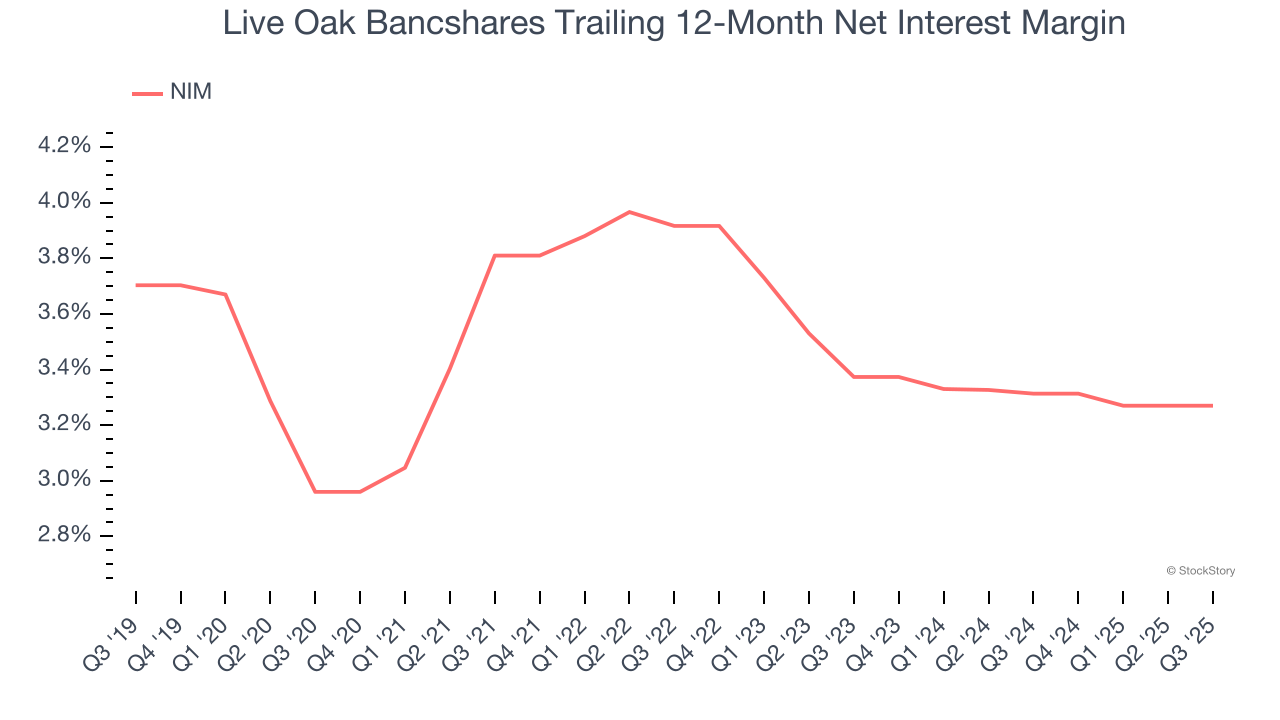

Low Net Interest Margin Reveals Weak Loan Book Profitability

Net interest margin (NIM) represents how much a bank earns in relation to its outstanding loans. It's one of the most important metrics to track because it shows how a bank's loans are performing and whether it has the ability to command higher premiums for its services.

Over the past two years, we can see that Live Oak Bancshares’s net interest margin averaged a subpar 3.3%, meaning it must compensate for lower profitability through increased loan originations.

Final Judgment

Live Oak Bancshares’s merits more than compensate for its flaws, but at $34.35 per share (or 1.4× forward P/B), is now the right time to buy the stock? See for yourself in our full research report, it’s free for active Edge members.

Stocks We Like Even More Than Live Oak Bancshares

Check out the high-quality names we’ve flagged in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.