Wrapping up Q4 earnings, we look at the numbers and key takeaways for the professional tools and equipment stocks, including Hillman (NASDAQ: HLMN) and its peers.

Automation that increases efficiency and connected equipment that collects analyzable data have been trending, creating new demand. Some professional tools and equipment companies also provide software to accompany measurement or automated machinery, adding a stream of recurring revenues to their businesses. On the other hand, professional tools and equipment companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

The 9 professional tools and equipment stocks we track reported a slower Q4. As a group, revenues missed analysts’ consensus estimates by 1% while next quarter’s revenue guidance was 0.8% below.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 6.1% since the latest earnings results.

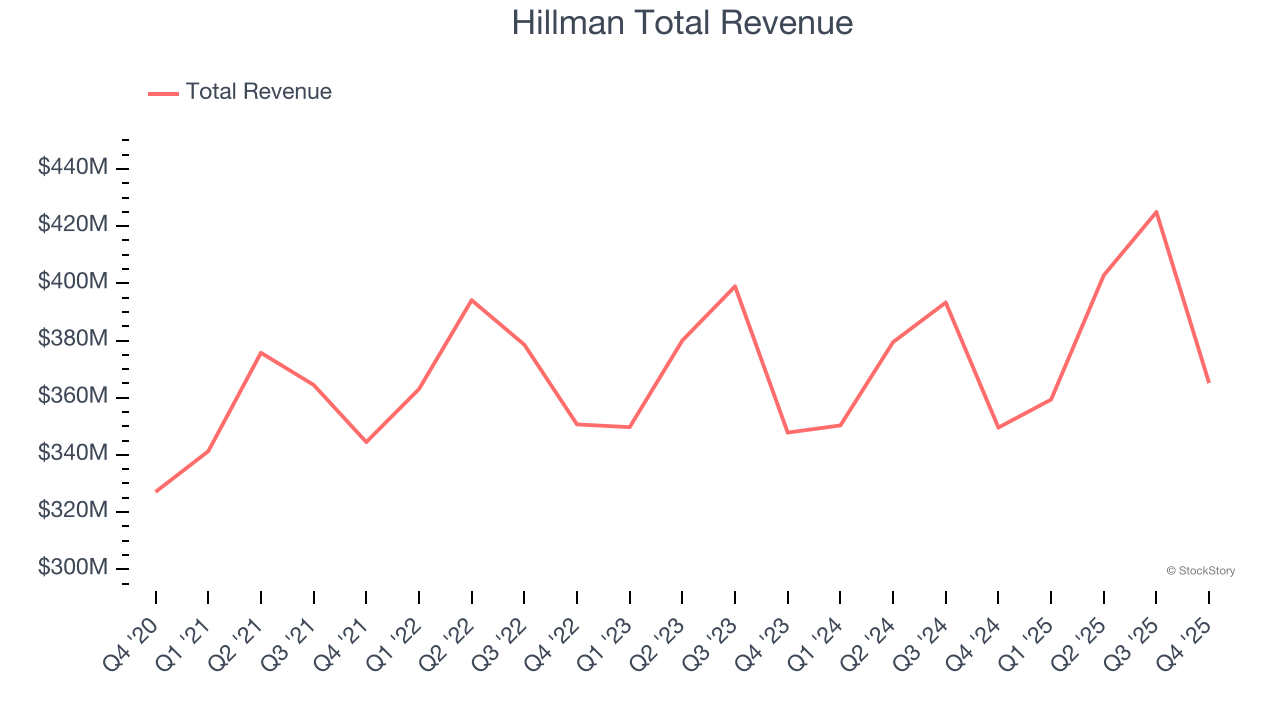

Hillman (NASDAQ: HLMN)

Established when Max Hillman purchased a franchise operation, Hillman (NASDAQ: HLMN) designs, manufactures, and sells industrial equipment and systems for various sectors.

Hillman reported revenues of $365.1 million, up 4.5% year on year. This print fell short of analysts’ expectations by 2%. Overall, it was a slower quarter for the company with a miss of analysts’ revenue estimates and full-year revenue guidance missing analysts’ expectations.

Jon Michael Adinolfi, Hillman's chief executive officer commented: “During 2025, we successfully managed the dynamic tariff environment while driving record top and bottom line results. The Hillman team did a great job this year taking care of our long standing partners and winning new business.

Hillman achieved the highest full-year guidance raise of the whole group. Still, the market seems discontent with the results. The stock is down 11.9% since reporting and currently trades at $8.29.

Read our full report on Hillman here, it’s free.

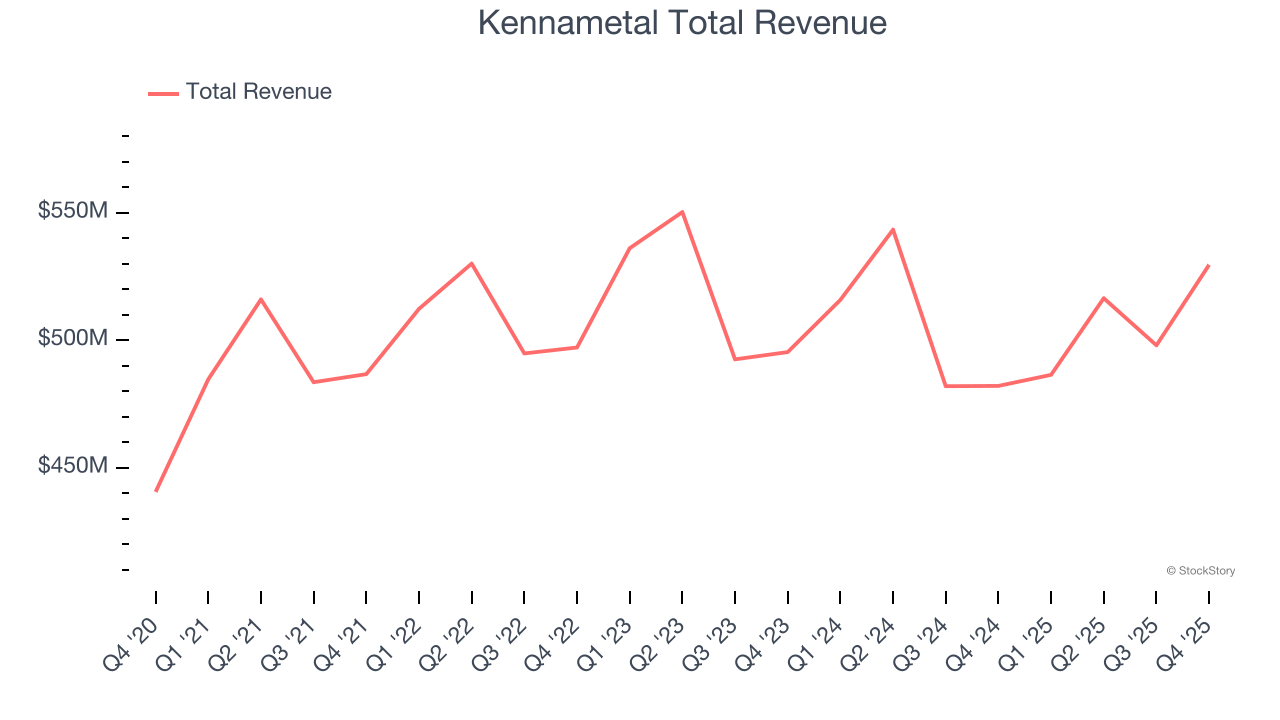

Best Q4: Kennametal (NYSE: KMT)

Involved in manufacturing hard tips of anti-tank projectiles in World War II, Kennametal (NYSE: KMT) is a provider of industrial materials and tools for various sectors.

Kennametal reported revenues of $529.5 million, up 9.8% year on year, outperforming analysts’ expectations by 1%. The business had a stunning quarter with an impressive beat of analysts’ EBITDA estimates and a solid beat of analysts’ adjusted operating income estimates.

Kennametal pulled off the fastest revenue growth among its peers. The market seems happy with the results as the stock is up 11.9% since reporting. It currently trades at $40.03.

Is now the time to buy Kennametal? Access our full analysis of the earnings results here, it’s free.

Middleby (NASDAQ: MIDD)

Holding a Guinness World Record for creating the world’s fastest conveyor pizza oven, Middleby (NASDAQ: MIDD) is a food service and equipment manufacturer.

Middleby reported revenues of $866.4 million, up 4.5% year on year, falling short of analysts’ expectations by 11.4%. It was a disappointing quarter as it posted full-year revenue guidance missing analysts’ expectations significantly and full-year EBITDA guidance missing analysts’ expectations significantly.

Middleby delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 4.8% since the results and currently trades at $150.28.

Read our full analysis of Middleby’s results here.

Lincoln Electric (NASDAQ: LECO)

Headquartered in Ohio, Lincoln Electric (NASDAQ: LECO) manufactures and sells welding equipment for various industries.

Lincoln Electric reported revenues of $1.08 billion, up 5.5% year on year. This result lagged analysts' expectations by 1.5%. Overall, it was a slower quarter as it also produced a significant miss of analysts’ organic revenue estimates and a slight miss of analysts’ revenue estimates.

The stock is down 8% since reporting and currently trades at $267.30.

Read our full, actionable report on Lincoln Electric here, it’s free.

Stanley Black & Decker (NYSE: SWK)

With an iconic “STANLEY” logo which has remained virtually unchanged for over a century, Stanley Black & Decker (NYSE: SWK) is a manufacturer primarily catering to the tool and outdoor equipment industry.

Stanley Black & Decker reported revenues of $3.68 billion, flat year on year. This number missed analysts’ expectations by 2.2%. It was a softer quarter as it also recorded full-year EPS guidance missing analysts’ expectations significantly and a significant miss of analysts’ revenue estimates.

The stock is down 10.5% since reporting and currently trades at $72.49.

Read our full, actionable report on Stanley Black & Decker here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.